08.0 - MANAGING COST ESTIMATING & BUDGETING

08.1 - Module 08-1 - Introduction to Managing Cost Estimating & Budgeting

08.2 - Module 08-2 - Develop Cost Estimating & Budgeting Policies & Procedures Manual

08.3 - Module 08-3 - Define The Estimates Purpose And Scope Of Work (Owner)

08.4 - Module 08-4 - Creating The Owners Cost Estimate (Top Down)

08.5 - MODULE 8-05 - DEFINE THE ESTIMATES PURPOSE AND INTERPRET THE SCOPE OF WORK (CONTRACTOR)

Given that for contractors, projects are profit centers and the reason contractors are in business is to make money from planning, executing and controlling projects, the sole and only purpose for a contractor to prepare an estimate is to win work, either through a competitive bidding process or through a negotiated contract. But the end result is always the same- winning more work.

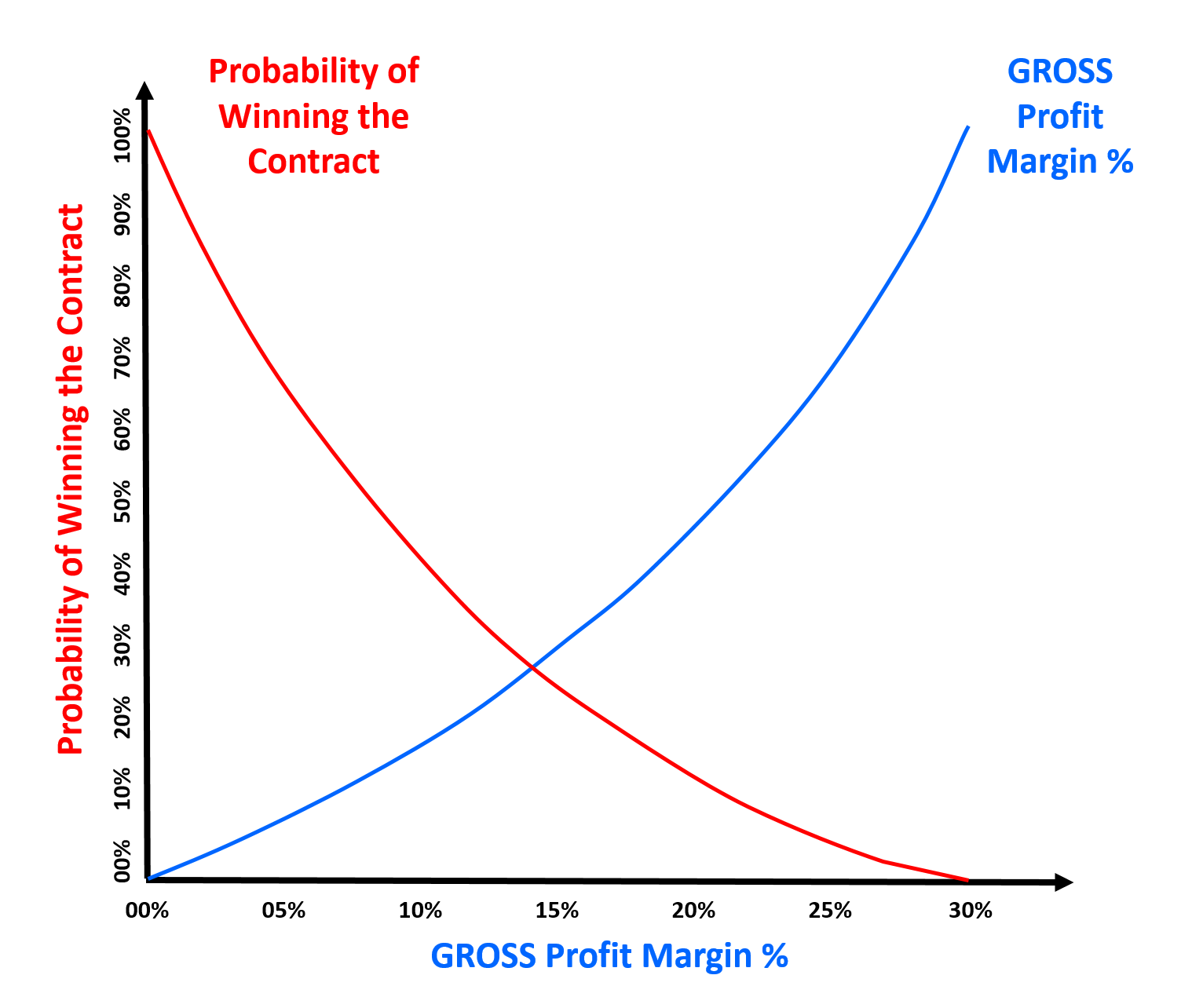

Before moving to the next topic, a quick review of accounting principles and terminology is in order. The gross margin is the Revenue – Cost of Goods Sold which are the project direct and project indirect costs. The project direct and indirect costs are also known as the “above the line” costs. Out of the Gross Profit, we also need to deduct the Home Office Overhead (known as General, Sales and Administrative costs) which gives us our Earnings Before Interest and Taxes (EBIT) which is also known as “Operating Income”. Some companies also use EBITDA, which is Earnings Before Interest, Taxes, Depreciation and Amortization. But whether your company uses EBIT or EBITDA, this is the money which is left over from the revenue stream and is known as NET INCOME.Whether competitively bid or negotiated, contractors are subject to the classic supply and demand curve:

Figure 1 - Probability of Winning vs. Profit Margin

Source: Giammalvo, Paul D (2015) Course Materials. Contributed Under Creative Commons License BY v 4.0

In this model, the probability of winning a contract is inversely proportional to the gross profit margin. To explain this simply, given no mistakes were made in the quantity take off, and given that all contractors purchase materials from the same or similar vendors and use the same or similar sub-contractors, the direct costs of a project are or at least should be essentially identical regardless of who builds it, meaning for a contractor, the only significant variable then becomes the project overheads and profit margin. In other words, the contractor who can best manage overhead expense, both on site and in the home office, is the contractor who has the competitive advantage. As we can see from the graphic above, at least theoretically, if the contractor reduced the gross profit to zero, he/she should have a 100% probability of winning the project. Why? Because by setting the gross margin to zero, the contractor is actually losing money on the project, because in the gross profit is included what is known as the “General Sales and Administrative (GS&A) costs, also called “below the line” costs.

Because the margins tend to be so slim, assuming the scope of work is well defined and does not contain too many conflicts, errors or omissions, the major decision for Contractor’s management to make is what the profit margin is. There are many variables which enter into the equation, but the most important are how much backlog of work the contractor has on the books currently and what does the economy look like in the next 2-5 years. These are the variables which usually determine what gross margin will be applied, because not only does the contractor have to cover his fixed (home office) overhead, he/she also wants to be able to keep key staff employed even if it means they are not working on projects but in the home office.

For more on bidding and bidding strategies, refer to Module 5.3 Tendering & Bidding the Project.

Figure 2 - Define The Estimates Purpose And Interpret The Scope Of Work Process MapSource: Guild of Project Controls

Figure 2 - Define The Estimates Purpose And Interpret The Scope Of Work Process MapSource: Guild of Project Controls

08.5.1 INTRODUCTION

While the OWNER has multiple purposes for a cost estimate, the Contractor essentially has one. To prepare a bid, which hopefully will be low enough to win a contract but high enough to still be able to make a profit appropriate to the risks the owner has placed on the owner via the contract documents.

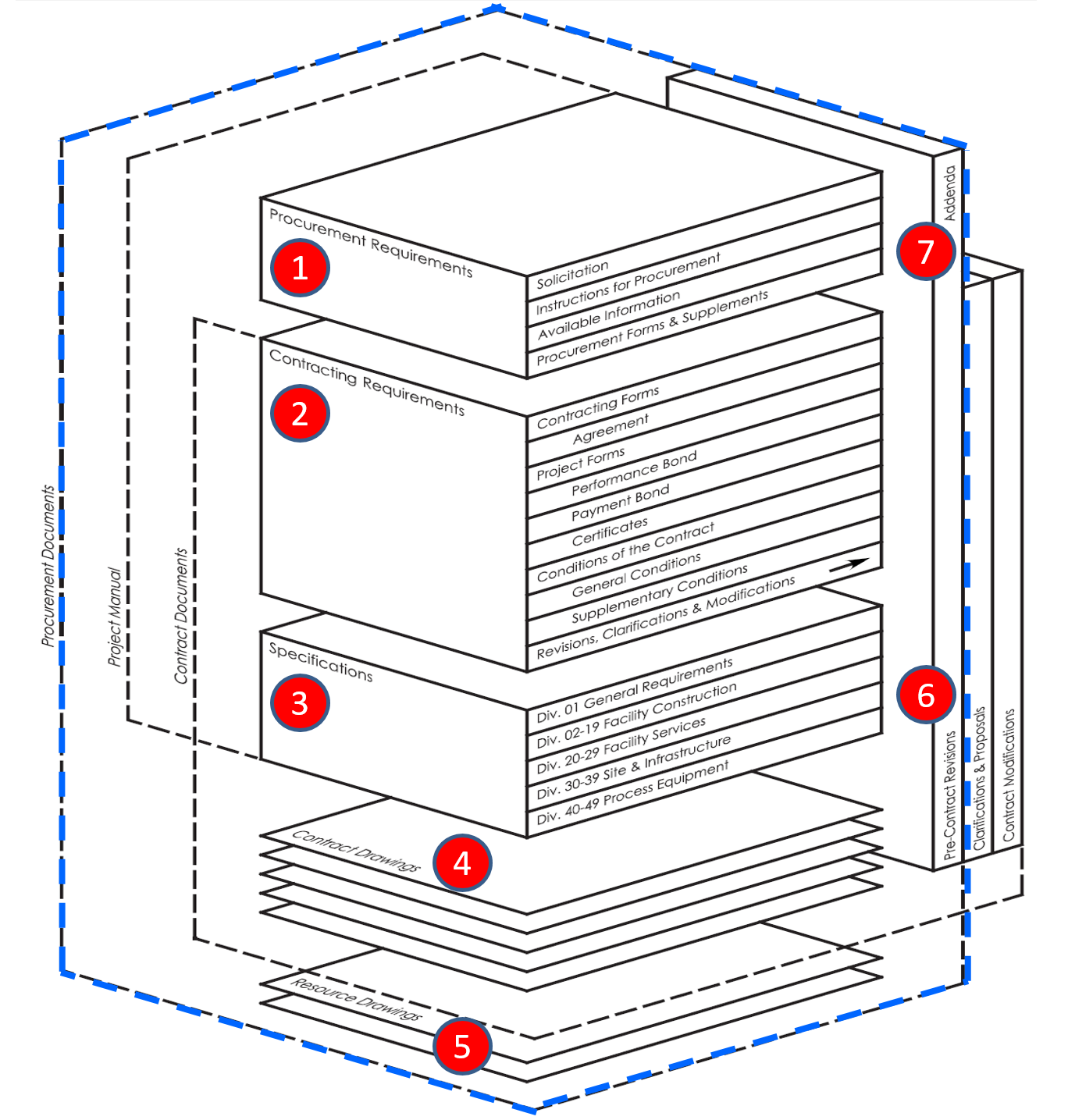

Figure 3 - Scope of Work Defined for the Contractor

Source: Construction Specifications Institute’s Manual Of Practice 5th Edition

For the CONTRACTOR, the scope of work is define first by the PROCUREMENT DOCUMENTS, which included or consists of:

(1) Procurement Requirements-

- Solicitation or Invitation to Bid

- Instructions to Bidders

- Available Information (e.g. Test borings, “As Built” drawing, Hydrologic Studies)

- Procurement Forms

(2) Contracting Requirements-

- Contracting Forms - i. Agreement (contract)

- Project Forms - i. Performance Bond, ii. Payment Bond, iii. Certificates of Insurance etc

- Conditions of the Contract - i. General Conditions, ii. Supplementary Conditions

- Revisions, Clarifications and Updates (See Items 6 and 7)

(3) Technical Specifications (written) (For more detail, see Omniclass Table 22- Work Results which takes the divisions below to 5 levels deep)

- Division 1- General Requirements

- Division 2-19 Facility Construction

- Divisions 20 – 29 Facility Services

- Divisions 30-39 Site and Infrastructure

- Divisions 40-49 Process Equipment

(4) Contract Drawings (“Blueprints”)

(5) Resource, Shop Drawings or Installation Instructions

(6) Pre-Contract Revisions/Clarifications

(7) Addenda

It is especially critical for cost estimators much more than planner/schedulers to fully immerse themselves in the contract documents, knowing and understanding what the owner is requiring, particularly as it applies to risks over which the contractor may have very little control or influence over.

This helps to explain WHY there is so much pressure on both owners and contractors alike to adopt standardized WBS and other coding structures, not only companywide but sector wide and even globally. Which is why the Guild of Project Controls is endorsing the use of Omniclass regardless of whether as owner or contractor you are using Building Information Modelling. (BIM)

08.5.2 INPUTS

- Contract Documents

- Historical Cost And Productivity Database (In-House Or Commercial)

- Bill Of Materials/Bill Of Quantities

- Cost Estimating Templates

08.56.3 TOOLS & TECHNIQUES

08.5.3.1 Team Cost and Scheduling Meetings

Because bidding work is a core competency of the contractor, and because the scope of work is to some degree or another, defined by the contract documents, contractors do not need to conduct the extensive stakeholder analysis required by owners.

Contractor Cost and Scheduling meetings are focused on HOW the contractors project managers and superintendents, along with key subcontractors and vendors plan on executing the work and what completive advantage might be had by investing in another piece of equipment or in adopting the latest methods. This is known as “constructability analysis” or “constructability reviews” where either an owner or a contractor applies value engineering tools and techniques to gain a competitive advantage over other bidders.

Explained another way, from the contractor’s perspective, cost and scheduling meetings are more about CONSTRUCTABIITY reviews. As contractors generally have established a standard way of working, contractor schedulers often use fragnets or even entire schedules from previous projects and simply adapt them to the current situation. As contractors have a well established database of productivity and costs unit costs derived from Activity Based Costing, meetings held by contractors are generally less formal and less frequent than those of owners, at least in preparing the bid.

The big meeting that is important to the contractor is the final presentation by the project manager or construction manager on how he/she plans on executing the work and what the work will cost which is done just prior to the contractor adding in their profit margin and submitting the bid. (See Module 5- Contracts)

08.56.3.2 Value Analysis / Value Engineering

Value Analysis/Value Engineering is defined to be:

“1.Manufacturing: Systematic analysis that identifies and selects the best value alternatives for designs, materials, processes, and systems. It proceeds by repeatedly asking "can the cost of this item or step be reduced or eliminated, without diminishing the effectiveness, required quality, or customer satisfaction?" Also called value engineering, its objectives are (1) to distinguish between the incurred costs (actual use of resources) and the costs inherent (locked in) in a particular design (and which determine the i ncurring costs), and (2) to minimize the locked-in costs.

2.Purchasing: Examination of each procurement item to ascertain its total cost of acquisition, maintenance, and usage over its useful life and, wherever feasible, to replace it with a more cost effective substitute. Also called value-in-use analysis.

The formula to calculate Value is: Value = (Performance + (Capability/Cost)) = Function/Cost

Put in the context of cost estimating, during this phase of the project’s evolution, we are trying to see if we can reduce or keep the costs and/or durations within the constraints and assumptions provided in the Decision Support Package. This may or may not be possible but if it is NOT, then we, as professional project control practitioners, have a professional if not a legal obligation to bring this to the attention of the appropriate decision makers. Failure to do so is, or should be, a serious ethical violation. Value Engineering can be used both by owners project controllers during the DESIGN phase of the project to come up with the most cost efficient DESIGN, while contractors typically apply Value Engineering tools & techniques as part of their “Constructability” reviews- trying to create a competitive advantage over other bidders by trying to figure out a way to do an activity or series of activities more efficiently or effectively.

For more reading on Value Analysis/Value Engineering below are three references:

- Duwal, Khakindra (2013) http://www.slideshare.net/khakindra/value-analysis-16193425

- Crow, Kenneth (2002) http://www.npd-solutions.com/va.html

- Society of Value Engineers (SAVE) http://www.value-eng.org/

08.5.3.3 Determine Level of Detail, Project Phasing, Weather & Other Constraints

In order to be able to ensure that all elements are “captured” or “identified” the following need to be considered and finalised if not already determined:

- DETERMINE LEVEL OF SCHEDULE DETAIL

Assuming that the owner has (as they should have) provided the WBS down to a minimum of Level 3 and preferably Level 4, the contractor has to determine whether to take the schedule down to Level 4, 5 or 6. As noted above as most contractors do the same or similar work over and over again, most contractors have developed fragnets or even whole schedules which they know have been tested and provide to work. All the contractor has to do is update the durations based on either the quantities provided by the owner (for those owners who use Quantity Surveyors) or based on the contractors own quantity take-off done manually or electronically using an electronic quantity take off digitizer.

Worth noting is that for those owners (or contractors) who adopt BIM, at least in theory the BIM software will do the quantity take offs automatically. However as we know from any software, there are bugs and many contractors still prefer to perform a selective quantity take off “the old fashioned way” at least on certain key items. (i.e concrete, excavation and piping are common elements checked and validated by the contractor prior to bidding)

- DETERMINE SEQUENCING OF PHASING

As contractors are not generally concerned with phasing, what the contractor is looking at is the sequencing and timing of work. As an example, in the cold climates, no contractor wants to be placing concrete in the winter months if at all possible as the costs of placing concrete in cold weather can often triple the unit in place costs. Same concept applies in places like the Middle East where you do not want to be placing concrete in the summer months as that too will increase the cost per unit in place. Other examples abound- working where there are typhoons or hurricane seasons, or working in the tropics where there are rainy seasons. All these are risk events that have an impact on productivity, thus duration and costs

- DETERMINE WEATHER PLANNING & OTHER MAJOR CONSTRAINTS

As noted above, there are many factors which act as constraints which the contractor needs to know and understand when bidding work. Some of the constraints are owner or government imposed, such as working in nuclear facilities or airports. Obtaining security clearances for your workers may take days or even weeks and gearing up to work in a nuclear facility may reduce effective productivity to only 30% to 50% of “normal” productivity.

08.5.3.4 Finalise Work Breakdown Structure & Control Accounts

The WBS is a scope (product or deliverable) oriented, hierarchical structure that defines all work required for the project at any given point in time and describes planned outcomes instead of planned actions. Explained another way, the WBS tells us WHAT needs to be produced, not HOW or WHEN.

Ideally, the WBS should be defined by the OWNER as that tells the contractor WHAT the owner needs or wants done which leaves it up to contractor to determine HOW and WHEN he/she will execute the work necessary to create each deliverable defined by the WBS Work Package.

Figure 4 - Excellent Example of what an OWNER should be providing to the CONTRACTOR in terms of summarizing the bid when submitted

Source: US National Park Service Cost Estimating Handbook (2011)

However if, the owner does not provide the WBS (and with the proliferation of BIM this will become increasingly LESScommon) then it will be up to the CONTRACTOR to create his/her own.

For most contractors working in North America, as CSI’s Master and Unformats have been around for over 40 years, most owners and contractors alike have learned to use them. (Which is why the US Park Service Templates are being used as an example of a “Best Tested and Proven” practice.) For those seeking additional sample WBS structures, turn to the GAO’s “Best Practices in Capital Budgeting” Appendix IX, page 328.

- TO CREATE A WBS, THE COST ESTIMATOR OR PROJECT CONTROLLER NEEDS TO IDENTIFY ALL SECTIONS, ELEMENTS AND PHASES OF THE PROJECT AND THEN ORGANIZE THIS SCOPE INTO A HIERARCHICAL STRUCTURE WITH EACH LOWER LEVEL OF THE STRUCTURE DEFINING ELEMENTS OF THE SCOPE OF WORKS ABOVE IT

08.5.3.5 Standardized WBS Structures

We know from Module 3 - Managing Scope that the three most well established STANDARDIZED WBS structures are:

(1) CSI’s Master and Uniformat for facilities

- Master Format - http://www.csinet.org/Home-Page-Category/Formats/MasterFormat/About-MF/…

- Uniformat

(2) Norsok Z-014 for offshore oil and gas-

(3) OmniClass Tables

- Masterformat Table 22 http://www.omniclass.org/pdf.asp?id=17&table=Table%2022

- Uniformat Table 2- http://www.omniclass.org/pdf.asp?id=6&table=Table%2021

08.5.3.6 Responsibility Assignment Matrix (RAM)

Most contractors do not bother with a Responsibility Assignment Matrix. As many contractors subcontract out some or even all the work on a project, the contract between the prime contractor and the subcontractors serves as the “responsibility assignment matrix”

In some organizations, a RAM is also called a “RACI Chart” (Responsible, Accountable, Consulted or Informed).

- For more on the topic of RAM and RACI documents refer to Module 2- Managing People

- BY MERGING THE WBS AND OBS, THE COST ESTIMATOR OR PROJECT CONTROLLER CREATES A RESPONSIBILITY ASSIGNMENT MATRIX OR RESPONSIBILITY BREAKDOWN STRUCTURE (RBS)

The RAM displays the lowest level of both the WBS and the RBS. The integration identifies specific responsibility (i.e. people) for specific project tasks (i.e. activities). In the Responsibility Assignment Matrix project work packages are associated with responsible persons (not departments) and each work packages shall have only one responsible person.

08.5.3.7 Cost Estimating Templates (Contractors)

There are any number of cost estimating templates for both owners and contractors available, either in “hard copy” (paper based) or more commonly, spreadsheets.

The best examples for both owner and contractor that the Guild has been able to locate in our research are the templates provided at no cost and under open source licensing are those offered by the US Parks Department.

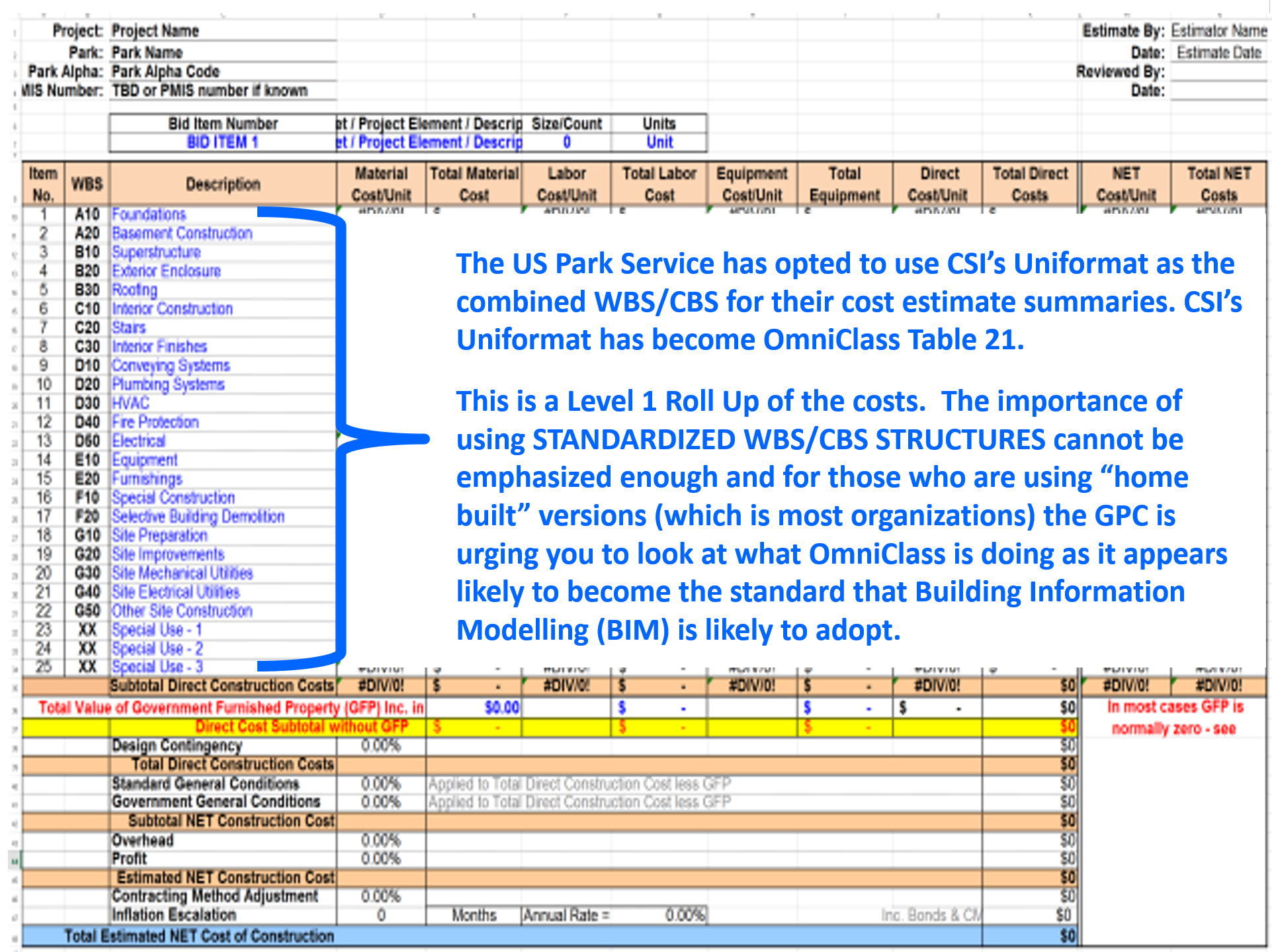

Figure 5 - Summary Level Cost Estimating Template

Source: US National Park Service Cost Estimating Handbook (2011)

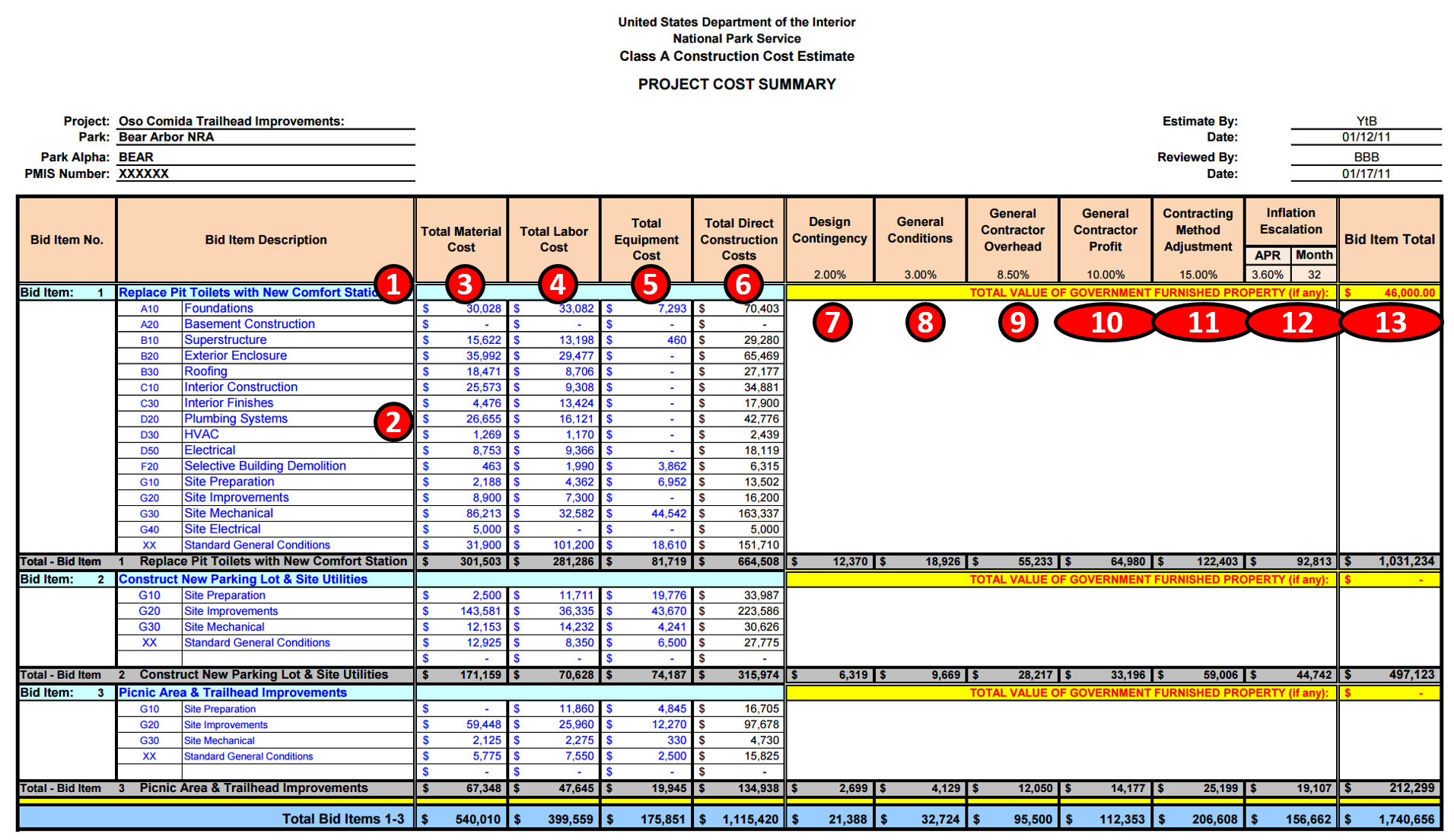

The example above shows what any cost estimating database should contain for information, whether Owner or Contractor:

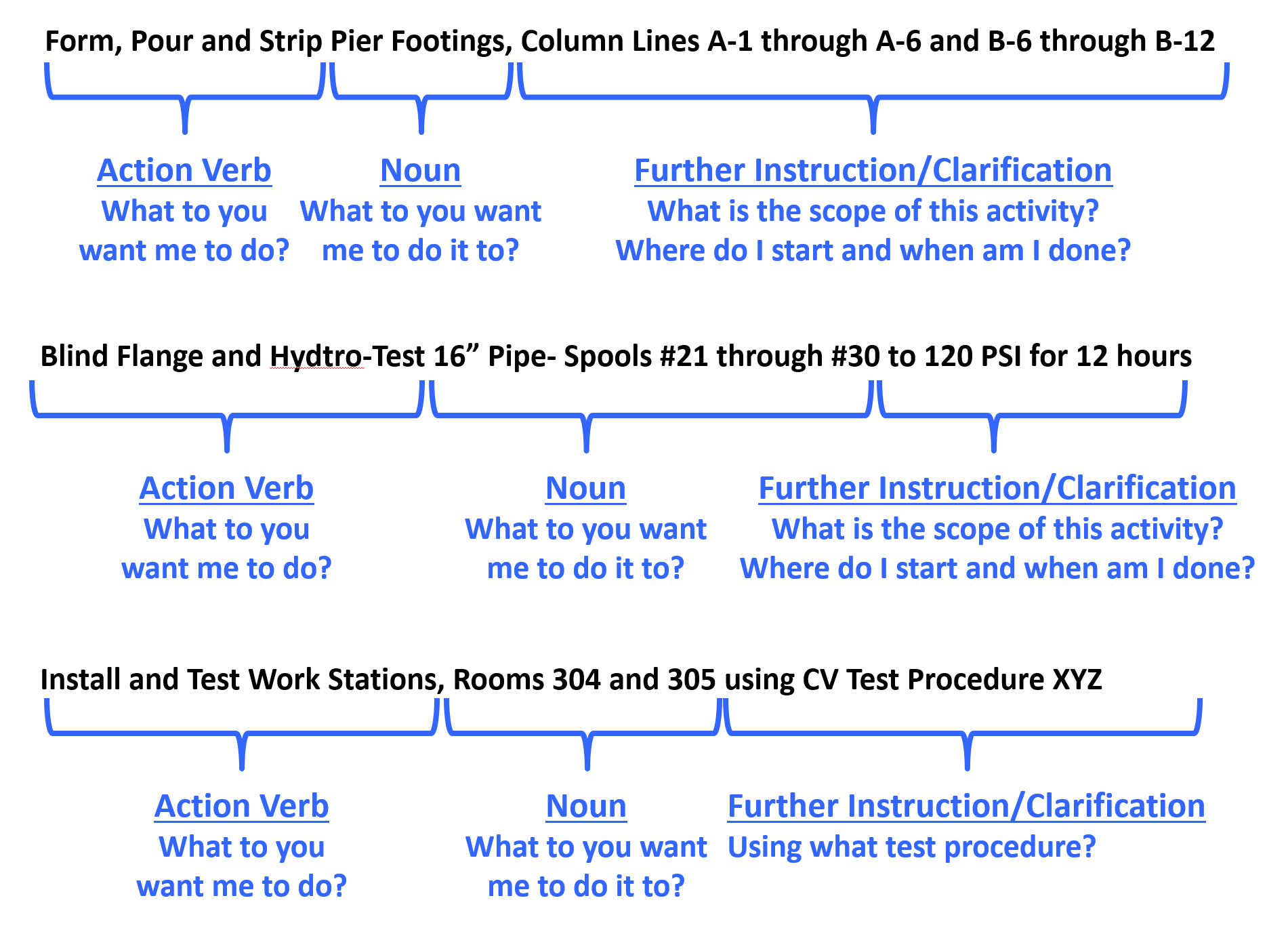

(1) Activity Name- Below are some examples of well-written Activity Names:

Below are some examples of well-written Activity Names:

Figure 6 - Well Written Activity Names

Source: Giammalvo, Paul D (2015) Course Materials. Contributed Under Creative Commons License BY v 4.0

However, in the example shown above because this is an owner’s cost summary, they rolled it up by bid items rather than by the more detailed activity names likely to be used by contractors or owners for any “self-performed” work.

(2) Coding Structure Sub Sort- In this case, the US Parks Department has opted to use CSI’s Uniformat as the basis to “roll up” their project costs.

For more examples of CSI Uniformat download this reference http://tinyurl.com/pwqofee which takes you to Level 3 of Uniformat for each of the main headings or you can download the Omniclass Table 21, http://tinyurl.com/pyk38jd which takes you to Level 5 for all headings (Figure 7 - CSI Uniformat Table 21 on the right, Source: Omniclass Tables (n.d.)).

Worth noting is that OWNER’s generally like using Uniformat/CSI Table 21 as it enables them to develop databases which are useful in the early phases of the project to develop cost estimates, while on the other hand, contractors tend to prefer using Masterformat/CSI Table 22 as it provides for much greater level of detail than does Uniformat.

(3) Material Cost- This should be self-explanatory but for cost estimators we need to be sure to check as materials prices vary significantly depending on location. The more remote the site, generally the more expensive materials are, because of shipping and storage costs.

(4) Labor Costs- Another largely self-explanatory heading but again, there are many factors which go into calculating labor costs, not the least of which is the actual productivity.

(5) Equipment Costs- Self-explanatory with the note that getting equipment to and from any given site (mobilization and demobilization costs) can often be significant and that has to be factored into the equipment costs along with the daily or hourly rental fee or cost of ownership.

(6) Total Direct Costs- Simply the sum of 3, 4 and 5 above. Now in this example above, because the contract is a cost plus type, the owner has every right to ask for and receive this information. However, if the contract was being let on a “firm fixed price” basis, then the owner would never see this level of detail. However, the contractor should have gone through the same process.

(7) Design Contingency- This is a RISK ALLOWANCE to cover the probability of design changes.

(8) General Conditions- This is what is known as the “Project Indirect” costs and covers things like the fencing/hoarding around the project, the site offices, electricity, fuel, QA/QC, Safety, Protective Equipment etc and other items identified in CSI Division 1/CSI Table 22 “General Conditions”.

(9) Contractors Home Office Overhead- This is a very real yet often contentious expense, which covers the salaries and facilities associated with the contractor’s home office. As this is generally considered a fixed expense, the percentage allocated to any project can vary, depending on the volume of work.

(10) Contractors Profit Margin- As noted previously, single digit EBIT margins are the norm for contractors around the world. So even if you go in with 10% target every mistake, error or omission the contractor makes comes out of that amount. Which is why we explain that for a contractor, his/her profit margin is the “Management Reserve”.

(11) Contracting Method Adjustment- This too is a “risk contingency” adjustment applied at the project level (as opposed to activity level) which covers such risk events as remote site construction, labor shortages/inefficiencies or working in adverse climates, either very hot and/or humid or very cold and dry. Again while it is unusual to see an owner organization recognizing this, if you are an owner’s project control professional then you need to recognize that this adjustment is or should be made by your contractors in putting together their cost estimate for bidding.

(12) Inflation Adjustment Factor- Again, self-explanatory with the caution that we tend to under-estimate what it really is. Given most governments lie about what the real or true inflation rate is in their country (the US underestimates inflation by a factor of 50%) the competent cost or project controls practitioner will take material and labor prices over a period of time and use those to project into the future what the real or true inflation rate is likely to be. Also for those who are working on International projects, don’t forget to factor in the exchange rate fluctuations. Many times those have a far worse impact than does inflation, especially in today’s global marketplace.

(13) Marked Up “Selling” price- This is a summation of the direct costs (6) plus the adjustments (7-11) to give us the CONTRACTORS SELLING PRICE which, when the work has been done and is billed by the contractor, becomes the OWNERS ACTUAL COST OF the WORK PERORMED (ACWP or AC)

Description of Mark Ups and Contingency (Cost Reimbursable Contract)

As for owners, a project is a cost or investment center, they do not mark up the price for profit, however, they DO need to mark up the quote the contractor submits to cover:

(1) Owner’s Project Management Overhead

(2) Owner’s Home Office Overhead (i.e. Finance charges)

(3) Owner Supplied Equipment/Materials or Services

(4) Owner Contingency (NOT Management Reserve as that does not belong to the project unless asked for and approved by management)

Keep in mind that for a contractor, the profit margin is their “management reserve”.

The Figure below also taken from R.S. Means 2008 Facilities Cost Estimating Database is typical for the USA. While other countries will undoubtedly vary, the concept remains the same. For cost estimators who are preparing costs for projects in countries other than their own, need to check to find out what the mark up requirements are for Labour especially.

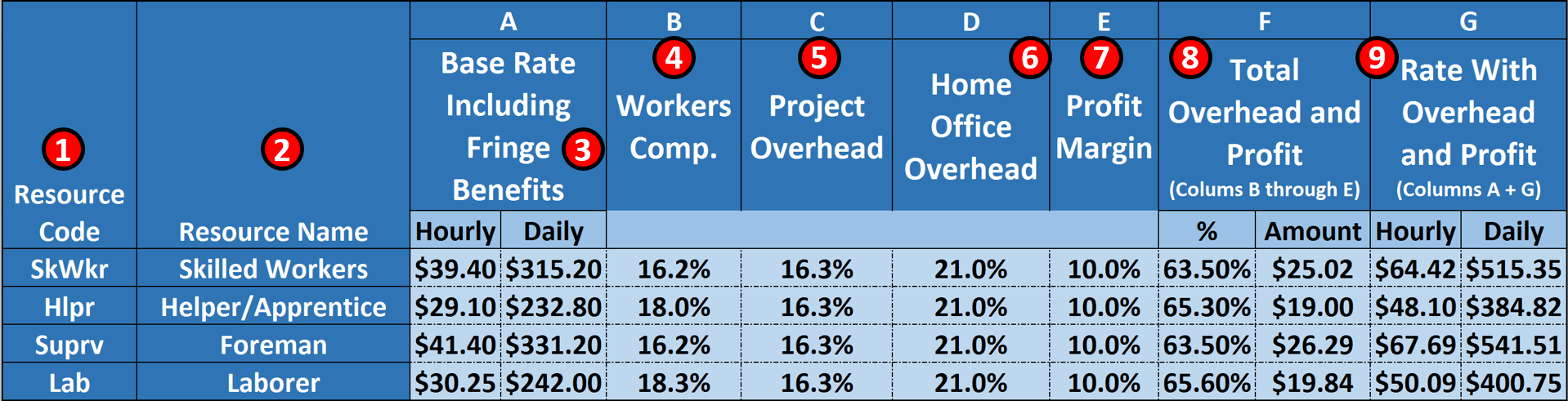

Figure 8 - R.S. Means 2008 Facility Cost Estimating Database Back Cover Showing Labour Rate Markups

Source: R.S. Means 2008 Facility Cost Estimating Database Back Cover Showing Labour Rate Markups

Explaining Figure 8 above-

(1) CODING STRUCTURE- as defined in the RESOURCE DICTIONARY. As with all other coding structures, it needs to be standardized to as great an extent as possible, not only within an organization but within an industry.

(2) RESOURCE NAME- This could be generic or it could be real people’s names

(3) BASE RATE- including fringe benefits (i.e. vacation, insurance) This is the taxable income as shown on your weekly or monthly pay stub.

(4) WORKER COMPENSATION INSURANCE- this insurance is to cover your expenses in the event you are hurt while working on the job.

(5) PROJECT OVERHEAD- are all the indirect costs directly attributable to the project but NOT identifiable to any single activity or work package. This includes the project manager’s salary, site offices, fuel for the vehicles, temporary heat, electricity and water. Basically any of the Division 1 (General Requirements) on the project. In accounting terms, these are often known as “above the line” or “Cost of Goods Sold”

(6) HOME OFFICE OVERHEAD- this is the owner’s salary and payroll for accounting, legal and the bidding team, the rent, heat, electricity and water for the home office. In accounting terms, these are known as “below the line” costs or General, Sales and Administrative expenses (GS&A)

(7) PROFIT MARGIN- which as has been noted, is normally targeted at 10% but often ends up less as for a contractor, this is his/her “management reserve”. Meaning if there are any “unknown-unknown” risk events that there was no budget or contingency allocated, the cost comes out of the profit margin.

(8) TOTAL OVERHEAD and PROFIT % is the sum of Columns 4-7 while

(9) Total OH&P Amount is the total % (8) X the Hourly Base Rate (3)

(10) HOURLY BILLING RATE is the amount from 9 plus the hourly billing rate from 3

(11) DAILY BILLING RATE is the Hourly Rate from 9 X 8 hour working day

08.5.3.8 Source of the Cost Data

For no other reason that R.S Means is probably the oldest (100+ years) and arguably has the largest or most complete databases, we have been using R.S. Means for our examples. (With their permission of course)

However, here are many other organizations who offer both general and specialized cost databases:

- SPONS- http://www.franklinandrews.com/publications/spons/

- Hutchins- http://www.franklinandrews.com/publications/hutchins/

- Griffiths- http://www.franklinandrews.com/publications/griffiths/

- Richardson’s- http://www.costdataonline.com/ Compass- http://www.compassinternational.net/

- Marshal & Swift- https://www.marshallswift.com/faq-43.aspx

From the perspective of practicality, instead of “reinventing the wheel” it is often preferable to purchase one of these commercial databases just for the structure and coding, and then modify the numbers to fit your area of operations than it is to try to create your own from scratch.

08.5.3.9 Assumptions / Constraints

Assumptions Our Business Dictionary defines “assumptions” to be “Accepted cause and effect relationships, or estimates of the existence of a fact from the known existence of other fact(s). Although useful in providing basis for action and in creating "what if" scenarios to simulate different realities or possible situations, assumptions are dangerous when accepted as reality without thorough examination. See also critical thinking and rule of thumb.

As cost estimators, we need to be asking “what assumptions are being made as the basis for this project moving forward? Examples of some common “assumptions” made in the evolution of projects in an owner’s organization are:

(1) Market Conditions- That the market will improve (or decline) resulting in favorable conditions for the project to produce a favorable return on assets or return on investment. For contractors, in times of little work (recessionary periods) they will often bid “at cost”, foregoing profits just to pay for their overhead and to keep their key employees working rather than laying them off. Owners need to keep this in mind as slow periods are the best time to perform CAPEX or OPEX funded projects as the bids will tend to be lower and the probability of manpower shortages will be reduced. Conversely, when times are good (non-recessionary periods) contractors can get away with increasing their profit margins and still winning bids but the risk is that manpower shortages result in them having to use less skilled/less productive trade professionals.

(2) Technology- That by the time this project is actually implemented, the technology selected for the project will not be technically obsolete.

(3) Resources- That there are there sufficient resources available (People, Machines, Money) to do this project. These are but a few examples of common assumptions which must be continuously challenged, tested and validated.

Constraints are defined to be an “Element, factor, or subsystem that works as a bottleneck. It restricts an entity, project, or system (such as a manufacturing or decision making process) from achieving its potential (or higher level of output) with reference to its goal. See also theory of constraints.

In the context of cost estimating and budgeting, a constraint is something which has been imposed upon us, either by a management decision or a reality that we have to accept. Some common examples of constraints which impact project controls professionals are unrealistic time durations- i.e. you cannot deliver a healthy baby in 9 months by impregnating 9 women and expecting a healthy baby in one month. Another common constraint is not recognizing and accepting that trying to shorten the time frame can be done at less costs. There is an optimum time to do every project and to try to do it very far from that optimum has cost impacts. Another very common constraint is the actual or real number of resources available to do the job who are competent.

08.5.3.10 Major Changes

Changes do not only happen during the Execution Phase of a project. Often change happens between one Phase Gate and the next- scope is added or deleted, equipment specifications change and thus we need to be tracking changes as the project evolves and this information needs to be captured in the Decision Support Package (DSP) which is the approval document to move from one phase gate to the next. Project Control professionals need to have access to these DSP’s as they contain a wealth of information that we need to know and understand.

What contractors need to be watching for during the BIDDING PROCESS are any Clarifications, Addenda or Modifications made AFTER the contract documents have been obtained by the contractor but BEFORE the bid is due. Failure to track and record all addenda, clarifications or modifications and incorporate those into the bid can result in some very unpleasant surprises come the bid opening.

While most standardized contract documents (i.e. FIDIC, AIA, EJCDC, Consensus Docs etc) have clearly defined process for contractors to follow in the event of a change, rarely do owners put in place anywhere near as robust a change control system internally. This will be covered in more detail in Module 14- Managing Project Change.

08.5.4 OUTPUTS

- Bid Or No Bid Decision

- Scope Of Work Understood

- Discrepancies, Errors, Omissions Or Conflicts In The Contract Documents Identified

- Cost Estimating Templates Approved/Accepted By Contractors Management

08.5.5 REFERENCES & TEMPLATES

- The US Government Accountability Office (GAO) “Cost Estimating and Assessment Guide- Best Practices for Developing and Managing Capital Program Costs” (2009) GAO-09-3SP http://www.gao.gov/new.items/d093sp.pdf

- US Dept of Energy (DoE) “DOE G 413.3-21, Cost Estimating Guide” https://www.directives.doe.gov/directives-documents/400-series/0413.3-E…

- Gary Cokins and the Institute of Management Accounts (2006) “Implementing Activity Based Costing” http://www.garycokins.com/images/pdfs/Cokins%20IMA%20SMA%20Implementing…

- United States Department of the Interior National Park Service Class A Construction Cost Estimate BASIS OF ESTIMATE- http://www.nps.gov/dscw/upload/classaconstcostestimatesample_1-26-11.pdf )

08.6 - Module 08-6 - Developing Contractors Cost Estimate (Bottom Up)

08.7 - Module 08-7 - Validate The Time & Cost Trade-Offs

08.8 - Module 08-8 - Validating Horizontal And Vertical Integration

08.9 - Module 08-9 - Conducting A Cost Risk Analysis

08.10 - Module 08-10 - Baselining And Communicating The Cost Estimate/Cost Budget

GPCCAR M08-5, Revision 1.01