08.0 - MANAGING COST ESTIMATING & BUDGETING

08.1 - Module 08-1 - Introduction to Managing Cost Estimating & Budgeting

08.2 - Module 08-2 - Develop Cost Estimating & Budgeting Policies & Procedures Manual

08.3 - Module 08-3 - Define The Estimates Purpose And Scope Of Work (Owner)

08.4 - Module 08-4 - Creating the Owners Cost Estimate (Top Down)

08.5 - Module 08-5 - Define the Estimates Purpose and Interpret the Scope of Work (Contractor)

08.6 - Module 08-6 - Developing the Contractors Cost Estimate (Bottom Up)

08.7 - Module 08-7 - Validate The Time & Cost Trade-Offs

08.8 - Module 08-8 - Validating Horizontal And Vertical Integration

08.9 - Module 08-9 - Conducting A Cost Risk Analysis

08.10 - MODULE 08-10 - BASELINING AND COMMUNICATING THE COST ESTIMATE / COST BUDGET

Figure 1 - Baselining and Communicating the Cost Estimate / Cost Budget Process Map

Source: Guild of Project Controls

08.10.1 INTRODUCTION

Now that the Cost Estimate / Cost Budget has been created and validated it needs to be "Baselined" in order to be used to communicate the "Oringinal Plan" along with "Current Progress" and "Future Forecasts" etc.

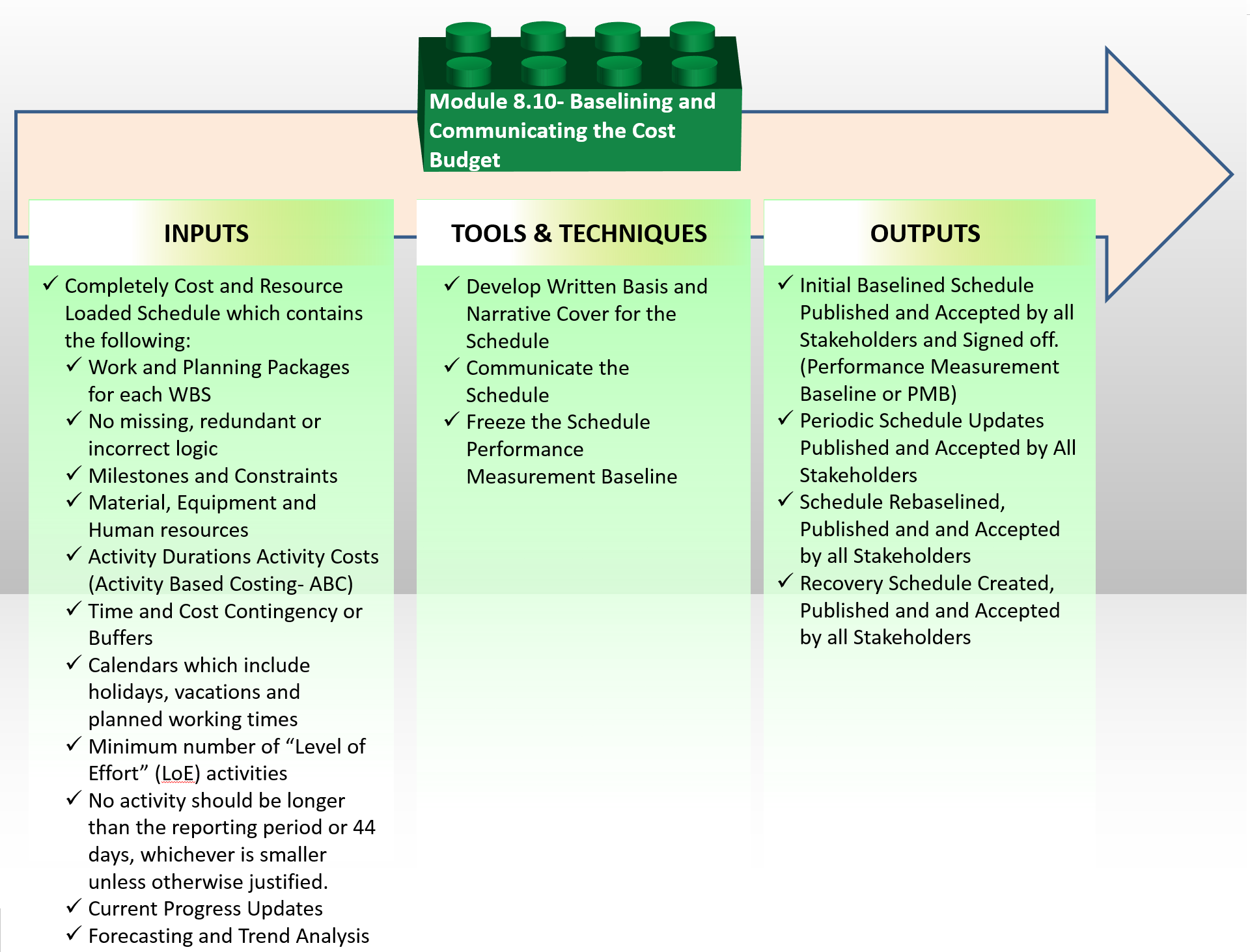

08.10.2 INPUTS

Completely Cost And Resource Loaded Schedule Which Contains The Following:

- Work And Planning Packages For Each Wbs Element (100% Of Necessary Activities)

- No Missing, Redundant Or Incorrect Logic

- Milestones And Constraints

- Material, Equipment And Human Resources

- Activity Durations Which Are Realistic And Achievable

- Activity Costs (Activity Based Costing- Abc)

- Time And Cost Contingency Or Buffers Appropriate To The Riskiness Of The Project, Work Package And/Or Activity

08.10.3 TOOLS & TECHNIQUES

08.10.3.1 Communicate the Cost Estimate / Cost Budget

This will often consist of an internal presentation / workshop or communication meeting whereby the scheduler is to communicate to the relevant stakeholders for the purposes of gaining acceptance of the schedule and the commitment and buy in of those who created it to executing what has been agreed to. This is often referred to very simply as “Plan your work then work your Plan” and if the plan is realistic, then there is no reason why it cannot be executed, provided a robust risk assessment was performed and appropriate risk contingency and buffers have been included.

- HAVING FINISHED YOUR COST ESTIMATE/COST BUDGET ANALYSIS, ADJUSTMENT AND OPTIMIZATION, THE PLANNER OR SCHEDULER WORKING WITH THE COST ESTIMATOR/PROJECT CONTROLLER SHOULD GAIN APPROVAL FROM THE RELEVANT PROJECT LEADERS TO OBTAIN BUY-IN FROM THE RELEVANT STAKEHOLDERS AND SPECIALISTS ETC.

To gain sign off internally or externally, a suitable Earned Value and / or Earned Schedule system would need to be documented and demonstrated.

To accomplish this, you would be expected to prepare the schedule and a summary or transmittal sheet containing the information above and then follow the communications process outlined and described in Module 2.3 - Communications in conformance with Module 2.5 - Identifying And Engaging Stakeholders.

To obtain acceptance, we need to refer to Module 3-5 - Accepting Completed Deliverables. For Contractors in addition to referring to Module 3.5, you also need to refer to Notice to Proceed and for Owner’s in addition to Module 3.5, you need to see Decision Support Packages as your project Cost Estimate/Cost Budget may not be a Level 4 Cost Estimate/Cost Budget destined for use by the contractor but a Level 1, 2 or 3 Internal deliverable.

For the CONTRACTOR as the cost and resource loaded schedule is normally a deliverable assigned to be provided by a specified date while on other projects it can be a prerequisite to obtain the Notice to Proceed or similar authorization to start work, Therefore the contractor has to submit the schedule for approval the same as any other submittal document.

For the OWNER, as the cost and resource loaded schedule is a key element of any decision support package, the owner’s project control team needs to submit for acceptance as part of the DSP approval process to move from one phase to the next. (See Module 3-6 - Accepting Completed Deliverables)

08.10.3.2 Develop Written Basis and Cost Estimate / Cost Budget Narrative

- DEVELOP A DOCUMENT TO SUBSTANTIATE, COMMUNICATE AND EXPLAIN THE SCHEDULE TO STAKEHOLDERS

An Executive Report and Cost Estimate/Cost Budget Analysis Report (Cost Estimate/Cost Budget Narrative) is required in order to demonstrate and document the underlying assumptions that are the foundation for the Cost Estimate/Cost Budget as well as providing an introduction to and synopsis of the Cost Estimate/Cost Budget.

In addition to utilising such a document to gain internal acceptance, signoff and / or project team acceptance and buy-in, the Cost Estimate/Cost Budget Analysis Report (Cost Estimate/Cost Budget Narrative) would also be required when the contractor submits the cost and resource loaded schedule as part of the approval or customer acceptance process. In this instance the contract documentation would likely specify the minimum information to be included in such a narrative.

It should include information that identifies the basis of the assumptions as to:

- Stakeholder coordination issues;

- WBS and Activity Sort / Filter Codes and their application;

- Content of Calendars and their application;

- Daily and weekly working hours, holidays and shift patterns;

- The critical path of the Contract;

- Near critical paths of the project;

- Content of Calendars and their application;

- Daily and weekly working hours, holidays and shift patterns;

- Assumed production outputs for all major activities and areas of the Works;

- An overall manpower forecast detailing individual trades and other sub-contract/indirect labour, commissioning teams and the like to illustrate the build-up of manpower resources.

- List of major items of plant or equipment that are required to be procured identifying the required procurement/mobilisation lead times, especially long lead time items;

- S-curves and histograms for resource or cost loaded schedules, major items of Contractor’s Equipment and manpower trades; and

- Any programme constraints, giving details of the constraints and the substantiation

08.10.3.3 Benchmark & Freeze the Schedule & Cost Performance Measurement Baseline

Once the project schedule is approved it becomes the benchmark or “Baseline” for the future project execution and control. A baseline schedule is the as-planned model of the scope of work for any project before its execution begins. As a baseline, it needs to be “frozen” and then used to compare future progress against the original plan, until such time as what is actually happening on the project is no longer consistent with the original baseline, at which time the schedule is either rebaselined or a “recovery schedule” is required.

There is a major difference between the Performance Measurement Baseline prepared by the owner vs the Performance Measurement Baseline prepared by the contractor is the contractor's PMB contains the contractor’s SELLING PRICE while the owner’s PMB contains their COST for these same activities. This seemingly small difference becomes important later on.

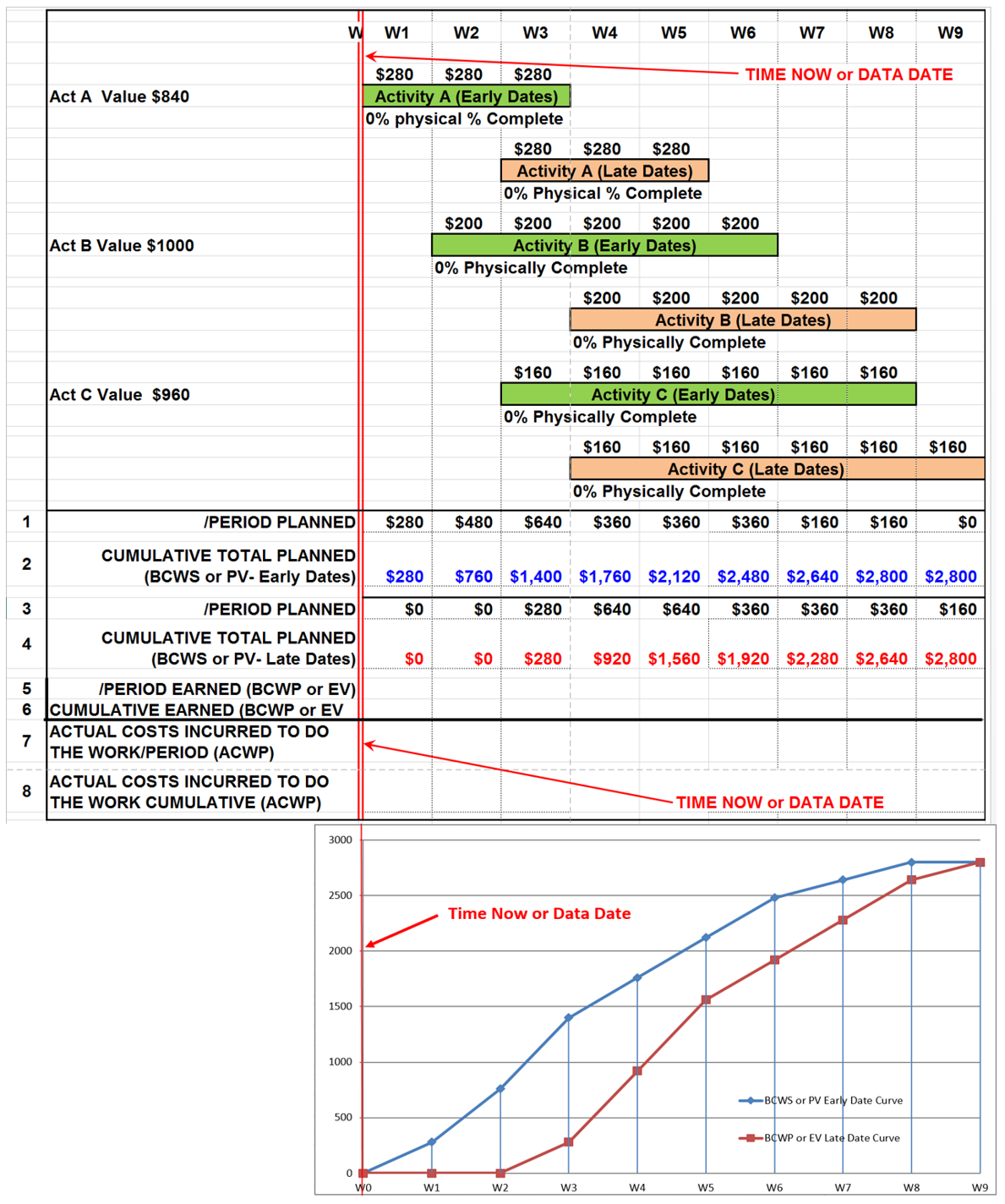

The Performance Measurement Baseline is most often is viewed as what is known as the “S” Curve and it should consist of not one but TWO curves which have been defined by the project’s Cost and Resource Loaded schedule:

- Early Date Curve - generated with all activities scheduled to start AS SOON AS POSSIBLE (ASAP)

- Late Date Curve - generated by constraining all activities to start AS LATE AS POSSIBLE (ALAP)

This is what the PMB should typically look like from both the owner and contractors perspective:

Figure 2 - Showing Owners Early and Late Date Curves vs Contractor’s Early and Late Date Curves

Source: Adapted from Humphrey's Gary (2015) Project Management Using Earned Value, 3rd Edition

The reason these curves are not the same is when the contractor SUBMITS the Cost and Resource Loaded Schedule to the owner for acceptance / approval the owner has to ADD to that schedule:

- Owner’s Management Activities (i.e. Project Management, Project Controls, Safety, QA/QC etc)

- Owner Supplied Equipment or Materials

- Owner’s Risk Contingency (i.e. both Time and Cost)

In Figure 3 below, using our Case Study developed in Module 08-6 - Developing The Contractors Cost Estimate (Bottom Up), we can see this is what the S-Curve or Performance Measurement Baseline (PMB) would look like coming from the CONTRACTOR to the OWNER. Once the owner has APPROVED and ACCEPTED this baseline, to make it of full value to the OWNER, the owner will have to ADD activities to cover:

- Owner’s Management Activities (i.e. Project Management, Project Controls, Safety, QA/QC etc)

- Owner Supplied Equipment or Materials

- Owner’s Risk Contingency (i.e. both Time and Cost)

Figure 2 - The S-curve

Source: Giammalvo, Paul D (2015) Course Materials. Contributed Under Creative Commons License BY v 4.0

By adding activities to cover these three additional items provided by the OWNER, and by extending the completion date to beyond the contractual completion date to cover owner’s testing and commissioning activities, will almost always result in the OWNER’S PMB being LARGER than that of the contractor as well as LONGER DURATION than the contractor’s PMB or S-Curve. This can be seen conceptually in both Figures 1 above and Figure 3 below.

To explain a different way, it is NOT a “best tested and proven” approach for the owner to track project performance against the contractors PMB alone. Why? Because without the OWNER capturing his/her own costs for work over and above the owners’ costs of the work done by the contractor, is going to give the owner an overly optimistic Cost Performance Index (It will usually remain at 1.0) and unless the Owner’s and Contractor’s completion dates are exactly the same (which also is not usually the case) it will give the owner an unrealistically optimistic SPI as well.

To see more on how to the OWNER can track their own costs against their PMB, see Module 09.3.3.2.2 Closing the Accounting Time Gap, Figure 11. Following this “best tested and proven” practice, the owner will be able calculate and use their own SPI and CPI which in most cases will NOT be the same as that of the contractor.

This is what the PMB should typically look like utilizing the Contractors PMB, Owner’s PMB and Owner’s Approved for Expenditure (AFE):

Figure 3 - Illustrating Contractors PMB, Owner’s PMB and Owner’s Approved for Expenditure (AFE)

Source: Giammalvo, Paul D (2015) Course Materials. Contributed Under Creative Commons License BY v 4.0

What the OWNERS “S” curve should NOT contain is undistributed money, known as MANAGEMENT RESERVE. For OWNER’s undistributed budget is NOT allowed to be included in the S Curve as it does not belong to the Owner’s project manager to spend, but as the name implies, belongs to the SPONSORING management who are free to allocate it as they deem appropriate, based on recommendations and / or requests from their project manager.

While CONTRACTOR’s are unlikely to ever see the OWNER’s S curve they both will be tracking project progress against the Contractor’s PMB, as the CONTRACTOR’s EARNED VALUE (BCWP or EV) becomes the OWNER’s ACTUAL COST of WORK PERFORMED (ACWP or AC) for the contractors activities. This will be covered in more detail below.

These curves are the cumulative cost of work scheduled based on the cost of each activity spread over time, which is known as “Budgeted Cost of Work Performed” (BCWS) or “Planned Value” (PV) How to cost load each activity and generate each of these three curves is covered in Module 8- Managing Cost Estimating and Budgeting.

The baseline will also demonstrate similar scurves which define the assumptions with respect to the demand for materials and / or manpower for the project etc. These, similar to the associated cost scurves will often be used for progress reporting and forecasting purposes once the schedule is baselined and progressed.

As the schedule is updated with progress, the timing of completed activities may differ from the originally planned dates, thus a copy of the non-progressed schedule must be retained for comparison purposes. This is the main purpose of the baseline – to demonstrate how the project plan would be executed.

Additionally, the remaining activities as they are completed will likely differ from the dates in the approved or agreed Baseline. By storing the Baseline dates and being able to utilise these as a static target against which to measure good and bad progress, the planner or scheduler and the project team have the ability to make decisions about mitigation of delay or improvement in implementation.

The process for this varies from software to software but essentially, you save a copy of the schedule with no updates and the data date showing the date at which it was baselined. This “clean” copy of the schedule should be archived by both owner and contractor. This archived copy should be sealed and not be used once it has been archived. As the CPM schedule can and often is used as evidence in arbitration and litigation, it should be treated with the same importance as any other contract document, with both “hard” (printed) and “soft” electronic version sent to the home office to be filed along with other contract documents on the project and both hard and soft copies kept on the job-site or in a separate secure location.

As it is or has the potential to be legal evidence, it should also be signed off as any other deliverable. For owners, a schedule, developed to a level appropriate to the phase gate, should be included in each Decision Support Package (DSP) for formal acceptance by the relevant managers before the project is officially sanctioned or funded.

For a contractor, a cost and resource loaded schedule is normally a prerequisite to obtaining the Notice to Proceed (NTP) and should be formally transmitted to the client just as any other submittal document, adhering to the transmittal process required in the contract documents.

For those working on internal projects (owner or contractor) you too should conduct a formal acceptance. One example of how an internal project schedule was accepted is it was posted on the wall and everyone involved signed their name to it. Ultimately, the key is to obtain ownership of the schedule and an honest commitment to meeting or beating it.

08.10.4 OUTPUTS

BASELINED COST & RESOURCE LOADED SCHEDULE ACCEPTED BY ALL STAKEHOLDERS AND SIGNED OFF CONTAINING THE FOLLOWING:

- A project overview or a general description of the project, including general scope and key estimated life cycle dates, and descriptions of each stakeholder, including the project owner, prime and subcontractors, and key stakeholder agencies.

- A general description of the overall execution strategy, including the type of work to be performed, and contracting and procurement strategies.

- A description of the overall structure of the IMS, including the scope and purpose of subprojects, those responsible for each subproject, the relationship between subprojects, a WBS dictionary, the status delivery dates for each subproject, and a list of key hand-off products and their estimated dates. In addition, it refers to relevant contract data requirements lists (CDRLs) and data item descriptions (DIDs) associated with schedules. Baseline Document Best Practice 10: Maintaining a Baseline Schedule Page 139 GAO-12-120G Schedule Assessment

- A description of the settings for key options for the relevant software, such as criticality threshold, progress override versus retained logic, and the calculation of critical paths and whether work progresses with duration updates.

- A definition and justification in the baseline document of all ground rules and assumptions used to develop the baseline, including items specifically excluded from the schedule. If rolling wave planning is used, key dates or milestones for detail and planning periods are defined.

- A justification of each use of a lag and date constraint that is clearly associated with the activities that are affected. Missing successor or predecessor logic is also justified.

- The documentation of each project, activity, and resource calendar, along with a rationale for workday exceptions (holidays, plant shutdowns, and the like), working times, and planned shifts.

- An explanation or rationale for the basic approach to estimating key activity durations and justification of the estimating relationship between duration, effort, and assigned resource units, to an appropriate level of detail.

- Definitions of all acronyms and abbreviations.

- A table of the purposes of custom fields. Any LOE activities in the IMS are clearly marked.

- A description of resources used in the plan and the basic approach for updating resource assignments, along with schedule updates and average and peak resource demand projections. The document defines all resource groups used within the schedule and justifies planned over allocations to an appropriate level of detail. In addition, key material and equipment resources are described in the context of their related activities.

- A description of critical paths, longest paths, and total float. A discussion of the critical paths, including justification for the criticality threshold, rationale for single or multiple critical paths, and justification for any gaps in a non-contiguous critical path. If the schedule has late date constraints, a description of the longest path is included. In addition, abnormally large amounts of total float are justified.

- A description of the critical risks as prioritized in a quantitative schedule risk analysis, along with a discussion of the appropriate schedule and cost contingency.

- A detailed description of the updating and schedule change management processes. Any additional documentation that governs them is referenced.

08.10.5 REFERENCES & TEMPLATES

- The US Government Accountability Office (Gao) “Cost Estimating And Assessment Guide- Best Practices For Developing And Managing Capital Program Costs” (2009) Gao-09-3sp Http://Www.Gao.Gov/New.Items/D093sp.Pdf

- US Dept Of Energy (Doe) “Doe G 413.3-21, Cost Estimating Guide” Https://Www.Directives.Doe.Gov/Directives-Documents/400-Series/0413.3-Eguide-21/View

- Gary Cokins And The Institute Of Management Accounts (2006) “Implementing Activity Based Costing” Http://Www.Garycokins.Com/Images/Pdfs/Cokins%20ima%20sma%20implementing%20abc.Pdf

- United States Department Of The Interior National Park Service Class A Construction Cost Estimate Basis Of Estimate- Http://Www.Nps.Gov/Dscw/Upload/Classaconstcostestimatesample_1-26-11.Pdf )

GPCCAR M08-10, Revision 1.02