03.0 - MANAGING SCOPE

03.1 - Module 03-1 - Introduction to Scope Management

03.2 - Module 03-2 - Developing the Scope Management Policies & Procedures Manual

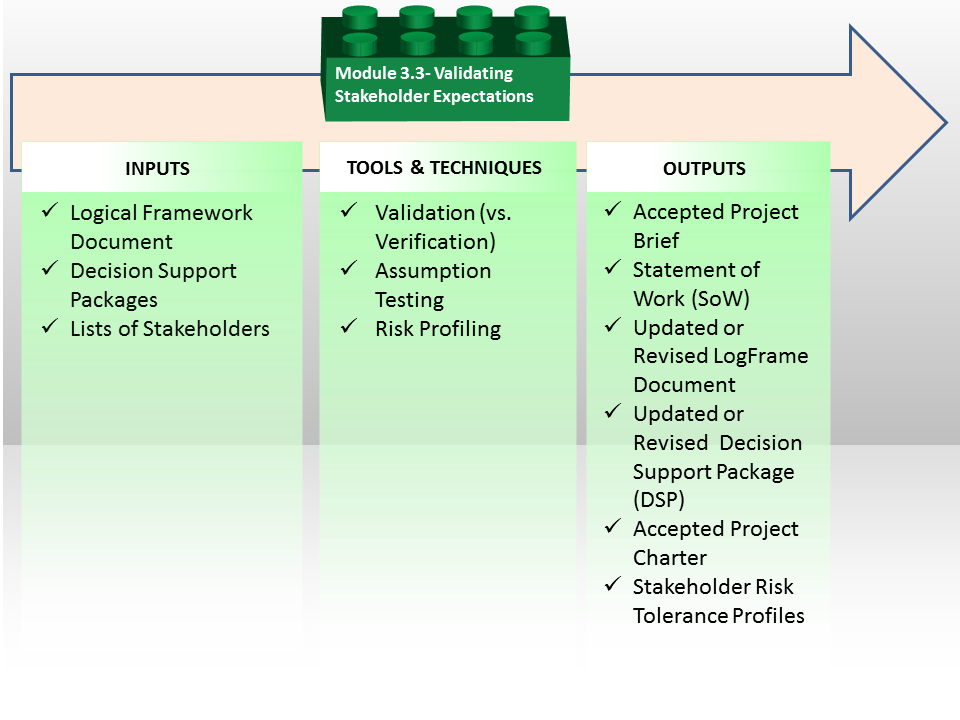

03.3 - MODULE 03-3 - VALIDATING STAKEHOLDER EXPECTATIONS

Figure 1 - Validating Stakeholder Expectations Process Map

Source: Guild of Project Controls

03.3.1 INTRODUCTION

As we know from Module 2-6, Identifying and Engaging Stakeholders the dictionary definition of “stakeholder” being used by the Guild is: “Any party that has an interest in an enterprise or project. The primary stakeholders in a typical corporation are its investors, employees, customers, contractors and suppliers. However, modern theory goes beyond this conventional notion to embrace additional stakeholders such as the community, government and trade associations.”

We also know that stakeholder management has become recognized as one of the major reasons projects succeed or fail and as project control professionals play such a key role in the collection, analysis and communication of project information, it becomes imperative that we know and understand the different perspectives to identify and engage stakeholders.

Lastly, we need to remember that Stakeholders fall into 6 generic categories and that in many cases, their needs, wants and expectations are contradictory, conflicting or in some cases, may even be mutually exclusive-

- Beneficiaries- Usually the customer client or end user of the product the project was undertaken to deliver. Those entities who will benefit from the product of the project

- Negative Beneficiaries- Those stakeholders who will either be negatively impacted TEMPORARILY while the project is executed (e.g. people who have to detour while new water pipes are being installed in their neighborhood) or PERMANENTLY. (e.g. Someone who lost their home to a new roadway being built)

- Implementers- Those leading or serving on the project team. This includes owner’s staff, contractor’s staff along with subcontractor and vendors. Anyone who provides support to the execution of the project.

- Decision Makers- The most obvious are the Asset Managers who act as SPONSORS for CAPEX funded project or Operations Managers who act as SPONSORS for OPEX funded projects. Other examples of decision makers would be the local building or electrical inspectors.

- Financiers- This includes the banks, shareholders, bond holders or those in the finance or accounting department.

- Regulators- These are any one of a number of Governmental or quasi-governmental agencies, including NGO’s. The prime examples are the Environmental Protection Agencies or the Board of Health. Any governmental agency which publishes rules or regulations which the project must comply with.

In the context of this Module (Managing Scope), this process applies primarily to OWNER’S Project Managers/Project Control Team and not to contractors. The only time a Contractor’s Project Manager/Project Control’s Team is likely to get involved is if the project is of the cost reimbursable type, such as Design-Build, Engineer, Procure, Construct and Commission (EPCC), Integrated Project Delivery (IPD) or Cost Plus Fixed Fee etc. where part of the contractor’s remit is to assist the owner in defining scope.

For the traditional “Design-Bid-Build” model (i.e. Firm Fixed Price or “hard money” contracting) the scope is the responsibility of the owner and/or the owners consulting team.

However, this is important for the well-rounded project control practitioner to know and understand as it is highly likely that in your career, you will end up working for both owner and contractor organzation's.

03.3.2 INPUTS

- List of Stakeholders Categorized By Type

- Initial Logframe Document

- Decision Support Package From Prior Phase Gate Reviews

03.3.3 TOOLS & TECHNIQUES

03.3.3.1 Validation (vs. Verification)

The initial action or responsibility to validate and verify any documented assumptions:

- Validation is the process of reviewing that the information provided by management or other key stakeholders via the LogFrame or Decision Support Documents is “reasonable and proper” while

- Verification is the process through which we measure and assess whether the project did or did not deliver what was expected, in the time frame required and to the quality specified or required. Given the fact that the project “success” rates are less than most organisations would wish for, one of the first responsibilities of the project controls practitioner is to validate that:

1) Time frames are “reasonable”

2) Cost budgets are “reasonable”

3) Risks are not “outrageous” and have been identified and addressed appropriately

4) Quality requirements are “consistent with the budget”.

In the event that we find that the stakeholder expectations are conflicting or otherwise unrealistic, we have to make this known to the relevant stakeholders.

03.3.3.2 Assumption Testing

Below are two ways practitioners can or should be testing and assumptions which have already been made and / or imposed upon them:

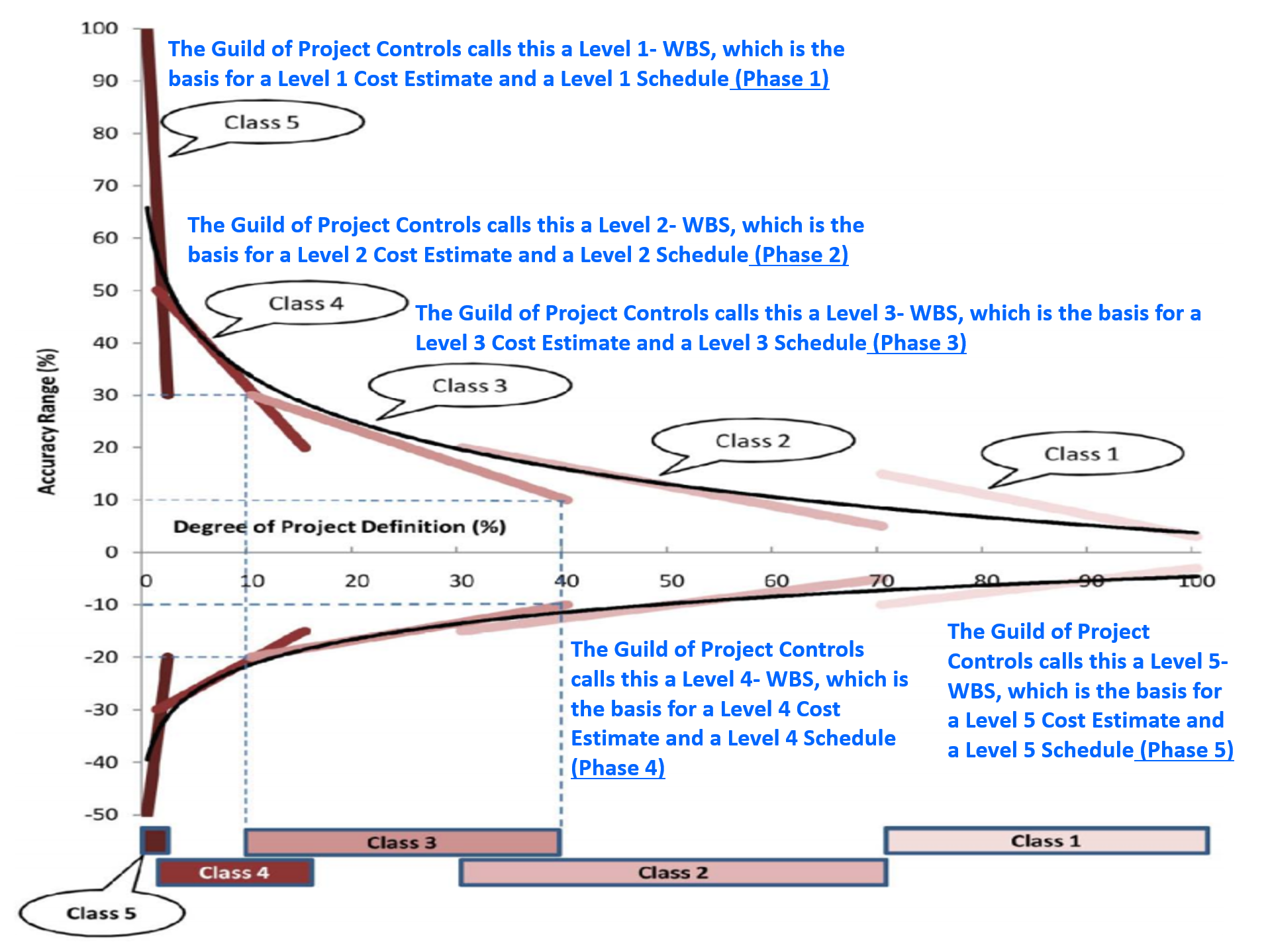

03.3.3.2.1 Acceptable “Range Estimates for Costs” at each given phase of a projects scope definition

The first graphic comes to us from the US Dept of Energy’s DOE G 413.3-21, Cost Estimating Guide and is based on AACE’s RP 18R-97. These values are typical of the process plant (oil, gas and mining) and as such, are indicative only and, unless other values have been specified, are a useful starting point:

Figure 2 - Showing Acceptable Ranges in Costs for each Phase of the Project Life Span

Source: Adapted from DoE Cost Estimating Guidelines

The values and ranges may vary from industry sector to sector and even from region to region. However, the concept remains valid as a “best tested and proven” approach and as practitioners in owner organizations only, we are obligated to at least prepare this kind of an assessment and present it to our management and / or other key stakeholders.

Because there is a strong correlation between scope, time and cost, it is critical that as owner project control practitioners, we test for assumptions in scope and to do that, we can use either time or cost as one of the tools & techniques test scope assumptions. As long as the cost and/or schedule is within the acceptable ranges for the phase we are in, is the means to validate whether our scope is reasonable.

To test for assumptions we compare the current cost estimate and/or duration against the target cost which is shown in Figure 2 above as the 0 or mean line as shown in Figure 2 above and/or against the Optimization Model shown in Figure 3 below.

To learn how to calculate and analyse these values, you need to refer to Module 4- Managing Risk & Opportunity, Module 7- Managing Planning and Scheduling and Module 8- Managing Cost Estimating and Budgeting.

- For those looking for paper topic or the more advanced certifications, given we know there is a correlation between costs and time on a project, developing the same kind of metrics shown below for acceptable ranges of cost estimates and adapting the concept to project durations would be a valuable and worthwhile contribution.

Once again, while this concept was developed for cost estimating the concept itself applies equally as well to Planning and Scheduling as it does to Cost Estimating.

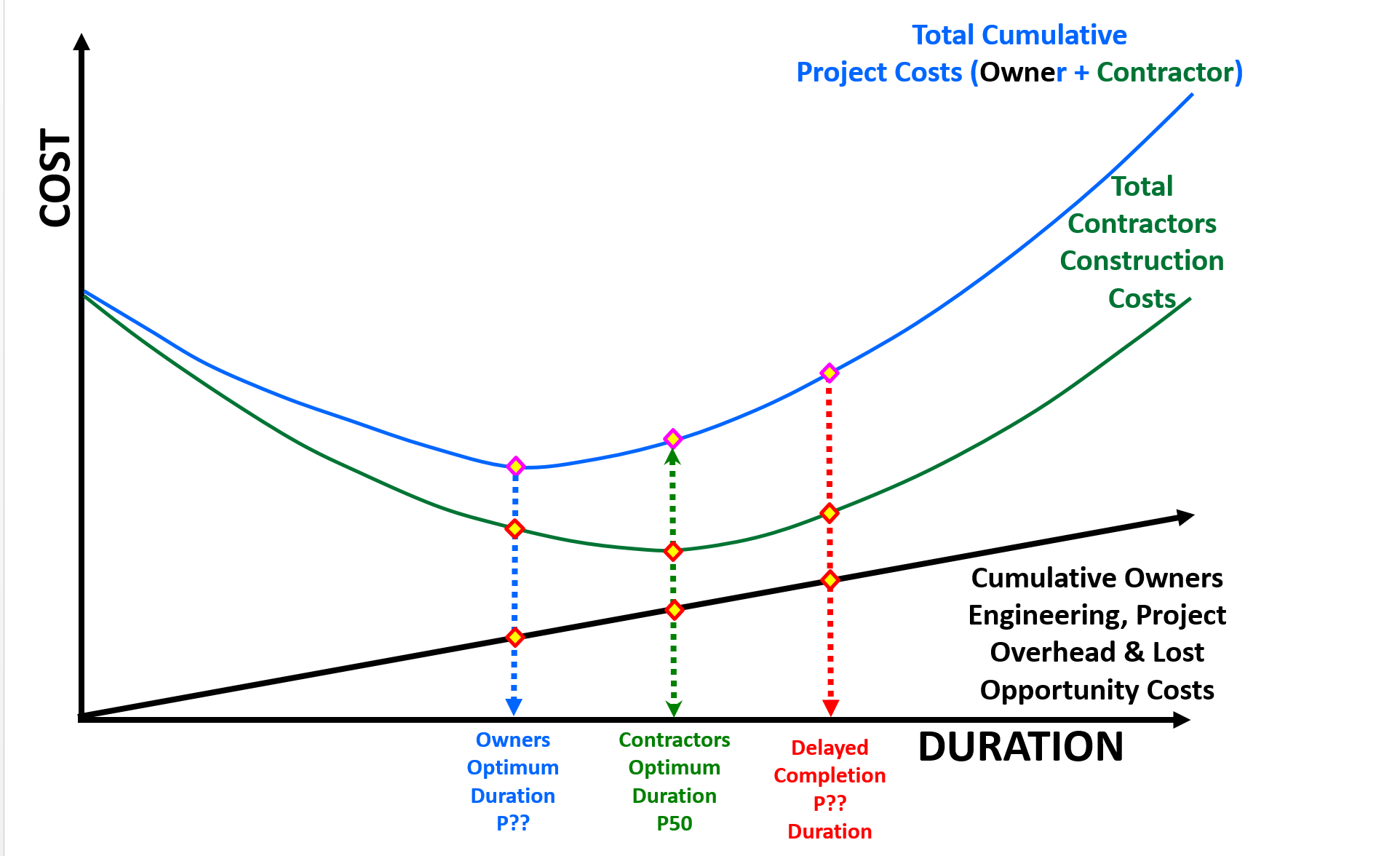

03.3.3.2.2 Has the scope been optimized as evidenced by the cost and duration estimates?

The second example comes to us courtesy of the US Dept. of Transportation’s Federal Highway Administration and shows conceptually how to calculate optimized trade-offs between time and cost. To actually learn the formula you need to go here US Dept of Transportation, Federal Highway Administration (2011) Work Zone Road User Costs - Concepts and Applications with the note that for private sector companies, you will need to SUBSTITUTE “Lost Opportunity Costs” in place of “Road User Costs”. And once again, this is NOT something contractors are likely to use UNLESS you are bidding on one of the Incentive type contracts. (See Module 5 - Managing Contracts to learn about these types of contracts)

- As noted above, given the fact that the correlation between time and cost is well known, a great paper topic for those seeking more advanced certifications would be to take many of the cost tools and techniques and adapt them for use in analysing schedule durations.

Figure 3 - Showing the Relationship Between Costs (variable, fixed and lost opportunity) and Duration

Source: Work Zone Road User Costs Concepts and Applications (2011) Figure 15 Page 116

Again, as this module is about ASSUMPTION TESTING, we can see from both figures above that if the calculated duration or costs do not meet acceptable criteria in terms of duration or cost, because there is such a strong correlation between scope, time and cost, we can use either or both durations or costs as one way to test to see if our assumptions fall within “reasonable” limits. Reasonable limits means if the cost estimate and/or budget falls outside of the acceptable ranges from the target duration or cost estimate, stands as prima facie evidence that our scope is either missing something or contains too much scope for the target cost or duration.

To learn how to calculate and analyse these values, you need to refer to Module 4- Managing Risk & Opportunity, Module 7- Managing Planning & Scheduling and Module 8- Managing Cost Estimating & Budgeting or you can go directly to the original source documents:

- DoE (2011) Cost Estimating Guide

- US Dept of Transportation, Federal Highway Administration (2011) Work Zone Road User Costs - Concepts and Applications

03.3.3.3 Risk Profiling

Our Business Dictionary defines “Risk Profile” as being “Threats” to which a company or organization are exposed. The risk profile will outline the number of risks, type of risk and potential effects of risks. This outline allows a business to anticipate additional costs or disruption to operations. Also describes the willingness of a company to take risks and how those risks will affect the operational strategy of the company. Thus another validation tool / technique we need to know and understand is the concept of Risk Profiling.

The reason this is important for the project control practitioner to know and understand is:

- if your stakeholders are risk AVERSE, then they may be reluctant or unwilling to accept your time or cost calculations unless you are using P90 values meaning cost or duration estimates which contain high amounts of CONTINGENCY.

- if your stakeholders are risk SEEKING, then you may find them pushing you to use P40 values meaning where not only is there no contingency but there is less than a 50/50 probability of the project finishing on or before the target duration and/or coming in at or under the allocated budget.

Explained another way, the risk profile becomes an input into many follow on processes, which is why it should be done as early as possible, before the WBS has been developed. Knowing and understanding the risk tolerances / expectations of your key stakeholders becomes of critical importance when calculating CONTINGENCY both in terms of time and cost.

Given the high ratio of projects which finish late and/or over budget, IF we want to raise the professional image of ourselves as practitioners, then we need to be able to “push back” against stakeholders who are either overly risk averse or recklessly risk seeking.

For high risk projects, both owners and contractors should seek out risk averse people.

- One of the responsibilities of the project control practitioner is to analyse whether the decisions being made are inconsistent with the risks of the project.

There are several methods we can take to measure or assess risk profiling in our stakeholders; one is through surveys and the second is using a Capital Asset Pricing Model (CAPM).

- Here is an example of a survey developed by the New Zealand State Government’s Risk Profile Assessment. The results of this survey should be included in the Decision Support Package or the LogFrame document to be used by the Project Control Practitioners when developing the WBS and other coding structures.

- The second example showing how developing a “Risk Profile” using the Markowitz Capital Asset Pricing Model can be used to help assess stakeholder risk profiles.

In both examples, the Project Control practitioner can use the information as the basis against which to assess the risk tolerances of the stakeholders and use that information to develop the WBS, Cost, Schedule and other information vital to making decisions on the project.

As the GPCCAR is a GUIDE and not designed to be the answer to all questions, for those seeking to learn more about the importance of risk profiling and how and why it should be included in a project controller’s tool box, first go to Module 4- Managing Risk & Opportunity OR here are additional supplemental references:

- Fina Metrica (2015) What is Risk Profiling

- UK’s Government’s Health and Safety Executive (n.d)

- Investopedia Definition of Risk Profile

03.3.4 OUTPUTS

- Accepted Project Brief

- Statement Of Work (Sow)

- Updated Or Revised Logframe Document

- Updated Or Revised Decision Support Package (Dsp)

- Accepted Project Charter

- Stakeholder Risk Tolerance Profiles

03.3.5 REFERENCES & TEMPLATES

- KPMG International (2017) Construction Survey

- Butts, Glenn (2010) Mega Projects Estimates- A History Of Denial?

- Butts, Glenn (2009) Joint Confidence Level Paradox (NASA)

- Flyvbjerg, Bent (2002) Underestimating Costs In Public Works Projects

- GAO (2009) Best Practices In Capital Budgeting

- DOE (2011) Cost Estimating Guide

- US Dept Of Transportation, Federal Highway Administration (2011) Work Zone Road User Costs - Concepts And Applications

03.4 - Module 03-4 - Creating the Work Breakdown Structure

03.5 - Module 03-5 - Creating the Control Accounts

03.6 - Module 03-6 - Accepting Completed Deliverables

GPCCAR M03-3, Revision 1.02