06.0 - MANAGING RESOURCE ACQUISITION / ALLOCATION

06.1 - Module 06-1 - Introduction to Managing Resource Acquisition / Allocation

06.2 - Module 06-2 - Develop the Resource Policies & Procedures Manual

06.3 - Module 06-3 - Acquiring Manpower for the Project

06.4 - Module 06-4 - Acquiring Materials for the Project

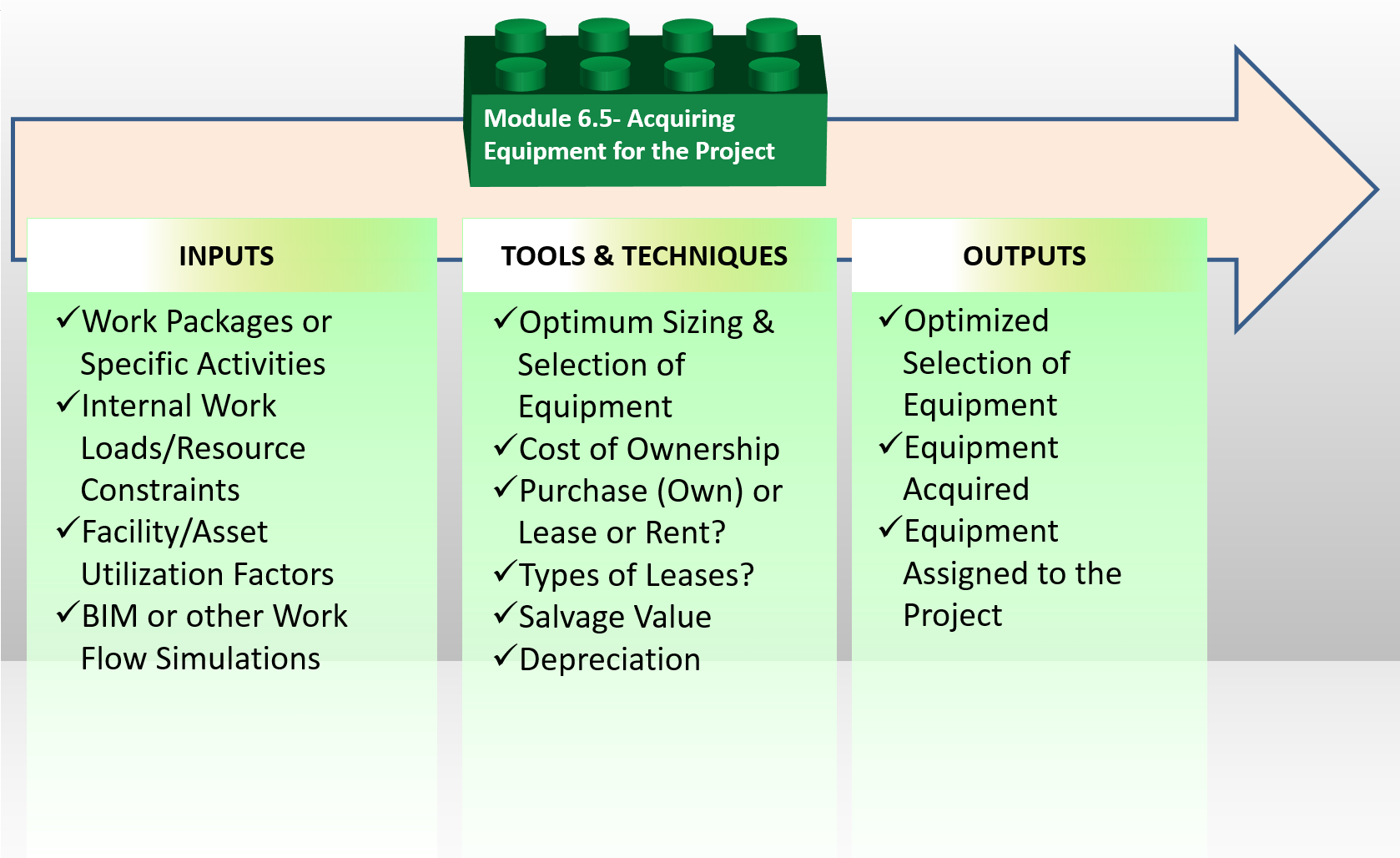

06.5 - MODULE 06-5 - ACQUIRING EQUIPMENT FOR THE PROJECT

06.5.1 - INTRODUCTION

Figure 1 - Process Map for Acquiring Equipment for the Project

Source: Guild of Project Controls

The process and procedure for acquiring equipment is identical to that to order materials, with a couple of additional steps and that is the fabrication of the equipment which of course makes equipment procurement much longer and thus more risky. This is why equipment is almost always identified as being a “long lead” items and especially on remote sites, are often ordered by the owner during the Phase 2 (“Assess) or “Phase 3 (“Select”) of the project. This is why so much time has been spend explaining the importance of “owner supplied equipment” or materials. Under these circumstances, the contractor is required to install, test and often commission the installed systems but the equipment itself is ordered, inspected, shipped, received and paid for by the owner, not the contractor. If the equipment is late, then it is up to the owner’s project control team to initiate expediting delivery. However, to do this, the contractor’s project control team must include owner supplied equipment procurement in their construction schedule and inform the owner’s project control team/project manager whether the equipment deliveries are likely to delay the project. Looking back to the leading cause of labour inefficiency we see that equipment shortages and lack of communications ranks in the top 11 causes.

From the contractor’s perspective, our focus as contractor project controls team is what equipment is going to be necessary, which activities will that equipment be needed for and how long will it take to get it from the vendor or your own yard to the site. Again, this is a process which the contractor’s project control team should have created a fragnet for and all you need to do is copy and paste it as a predecessor to the relevant activities and you are done.

As a contractor’s project control practitioner, your primary contribution is to calculate what the optimum size is and number of pieces of equipment are necessary. In some organizations this is done by the planner/scheduler while in others it is done by the cost estimator, but regardless of who does it, someone needs to take responsibility either to do it or to make sure it gets done. The reason for this is having the appropriate size and number of equipment has as direct impact on the duration of each activity as well as the costs of those activities- not only the direct costs but the overhead costs as well.

06.5.2 - INPUTS

- WORK PACKAGES OR SPECIFIC ACTIVITIES

- INTERNAL WORK LOADS/RESOURCE CONSTRAINTS

- FACILITY/ASSET UTILIZATION FACTORS

- BIM OR OTHER WORK FLOW SIMULATIONS

06.5.3 - TOOLS & TECHNIQUES

06.5.3.01 - Optimum Sizing & Selection of Equipment

For the purposes of the GPC exams, it is unlikely you will get a question requiring you to actually calculate the optimum sizing of equipment, or the productivity of that equipment, however, as a project control practitioner you need to know where to look to find this information as you will undoubtedly have to use it at some point in your career. This is the kind of task often assigned to junior planner/schedulers or cost engineers. Meaning for the Foundation level exams you need to KNOW and UNDERSTAND what resources you would start with in the event your boss assigned you to perform these calculations.

It is important for the project control practitioner to know and understand how to calculate or optimize the number of pieces of heavy equipment necessary to perform a given task. The reason it is important is if you have an activity which is so many days long and you know what heavy equipment is available, you may find out that the equipment available is not able to perform the work in that time frame.

Conversely, you may be asked given a specific duration and an estimated scope of work, (say cubic meters of excavation) what equipment or combinations of equipment are going to be required to execute the scope of work within the durations estimated.

The reason this has relevance to both planner/schedulers as well as cost estimators/budgeters is because optimizing the equipment to the task not only impacts the duration of that task or work package but also the costs associated with that task or work package. While this responsibility should be that of the design engineer responsible for the work, the truly professional project controller double checks to make certain that this has been done.

Below are some examples of papers and other resources to help you understand where to look if you are assigned this kind of task. To start with, the major equipment vendors all offer white papers which will help you identify which pieces of equipment are appropriate for your specific needs as well as both the productivity of each machine as well as the costs of ownership and maintenance.

e-Books-

- Construction Equipment Management for Engineers, Estimators, and Owners by Douglas D. Gransberg, Calin M. Popescu, Richard Ryan (2006) Chapter 5 http://tinyurl.com/q39dsrn

- Caterpillar-Caterpillar Performance Handbook Edition 29 http://nees.ucsd.edu/facilities/docs/Performance_Handbook_416C.pdf

- Caterpillar® Equipment Selection and Application Guides https://www.holtcat.com/Documents/PDFs/waste/Waste%20Landfill%20CAT%20E…

- Volvo- Product Range Guide http://www.volvoce.com/SiteCollectionDocuments/VCE/Documents%20North%20…

- Komatsu- Equipment Selection Guidelines http://www.komatsuamerica.com/equipment/excavators/miningexcavatorsshov…

- Komatsu Product Information http://www.komatsu.com/ProductInfo/ E-publications and E-zines

- Equipment World- http://www.equipmentworld.com/white-papers/

- Construction Equipment http://www.constructionequipment.com/equipment-executive-challenge-opti…

- Construction Equipment Guide- http://www.constructionequipmentguide.com/pages/charts.asp

Published Papers-

- Equipment Selection for Surface Mining: A Review Christina Burt Department of Mathematics and Statistics, University of Melbourne, Melbourne, Australia Lou Caccetta Department of Mathematics and Statistics, Curtin University of Technology, Bentley, Australia [email protected] http://www.optimization-online.org/DB_FILE/2013/04/3831.pdf

06.5.3.02 - Cost of Ownership

While planners and schedulers need to know and understand how to calculate and optimize equipment productivity for the purposes of establishing activity or work package durations, cost estimators have a much more challenging job of calculating the Total Costs of Ownership (TCO) of a piece of equipment and then using that information to make the decision whether it is better to own, rent or lease a piece of equipment.

Total Cost of Ownership (TCO) is an analysis meant to uncover all the lifetime costs that follow from owning certain kinds of assets. For this reason, TCO is sometimes called life cycle cost analysis.

Ownership costs include all of the following 15 categories of cost elements:

(1) Purchase cost: The actual price paid for equipment.

(2) Maintenance costs: warranty costs, maintenance Labour, contracted maintenance services or other service contracts.

(3) Acquisition costs: the costs of identifying, selecting, ordering, receiving, testing and commissioning the equipment in order for it to be used.

(4) Upgrade / Enhancement / Refurbishing/Rebuilding costs.

(5) Reconfiguration costs. Especially true for any pieces of equipment using GPS control systems

(6) Set up / Deployment costs: costs of configuring space, transporting, installing, setting up, and integrating with other pieces of equipment. i.e. in order to optimize a new excavator, will require the purchase of an additional dump truck.

(7) Operating costs: for example, human (operator) Labour, energy/fuel/hydraulic oil and filter costs.

(8) Change management costs: i.e. costs of operator orientation, operator training, workflow/process change design and implementation.

(9) Infrastructure support costs: i.e. costs incurred to garage and maintain the equipment, including spare parts, filters and other consumable costs

(10) Environmental impact costs: i.e. costs of waste disposal/clean up, or pollution control, or the costs of environmental impact compliance reporting.

(11) Insurance costs.

(12) Security costs: a. Physical security, for example, security additions for a building, including new locks, secure entry doors, closed circuit television, and security guard services. b. Electronic security, for example, security software applications or systems, offsite data backup, disaster recovery services, etc.

(13) Financing costs: for example, loan interest and loan origination fees.

(14) Disposal / Decommission costs.

(15) Depreciation expense tax savings (a negative cost).

Calculating the total costs of ownership depend on the decision of what “life span” of the equipment to use:

(1) Depreciable life: The number of years over which an asset will be depreciated. In each year of this life, a depreciation expense is calculated (as prescribed by local tax laws and accounting standards), which lowers reported income with the intent to create tax savings. (investment incentives)

(2) Economic life: Period over which an asset (machine, property, computer system, etc) is expected to be usable, with normal repairs and maintenance, for the purpose it was acquired, rented, or leased. Expressed usually in number of years, process cycles, or units produced, it is usually less than the asset's physical life, and is the period over which the asset's depreciation is charged. Also called average life, service life, effective life, mean life, or useful life.

(3) Service or Useful life: Period during which an asset or property is expected to be usable for the purpose it was acquired. It may or may not correspond with the item's actual physical life or economic life.

(4) Physical Life: The amount of time that a valued instrument has to perform business operations, like a piece of equipment. Explained another way, how long will a piece of equipment, correctly maintained physically last before it becomes unusable.

When calculating the Total Cost of Ownership, it is important that you determine which life you will use as the basis for your calculations as these lives are not the same duration. To remedy that problem often the calculations will be based on a set number of years- say 10 or 15. The other option is to set the life at the Service or Useful life.

06.5.3.03 - Purchase (Own) or Lease or Rent?

There are three common ways for either an owner or contractor acquire equipment. The first is we can PURCHASE it and the second is we can LEASE it or if only for a short period of time, we can RENT it.

The definition of LEASING is Written or implied contract by which an owner (the lessor) of a specific asset (such as a parcel of land, building, equipment, or machinery) grants a second party (the lessee) the right to its exclusive possession and use for a specific period and under specified conditions, in return for specified periodic rental or lease payments. A long-term written lease (also called a deed) creates a leasehold interest which in itself can be traded or mortgaged, and is shown as a capital asset in a firm's books.

Advantages of leasing include:

(1) lack of restrictive covenants (common in bank loans and bond indentures),

(2) conservation of capital (because the lessor provides 100 percent financing),

(3) tax savings (in most cases),

(4) avoidance of the risk of obsolescence, and

(5) relative ease of obtaining a lease as opposed to a comparable bank loan.

In most cases a lease, in effect, is a hire-purchase agreement without the requirement of an initial deposit and the added advantage of tax benefits.

The definition of RENTING is “Renting typically involves a shorter time period, often 1 year maximum, with the option to extend after the term at the discretion of both parties. Rentals are more suited to the temporary use of assets (land, buildings, or machinery) when the expectation is that it will not be needed long term. Rental contracts are generally far more casual than lease agreements, where a formal agreement with many terms will be drawn up.

Alternatively, if the cost of renting/leasing the asset is high it can be rented for a short period only when absolutely needed and then returned. Often this happens with construction work, where a very expensive piece of equipment (i.e. a crane) is needed for a relatively short time period but not afterwards. There’s no need to buy the asset or even lease it for several years, so a short rental period is appropriate.

Rental costs are always expensed on the income statement for both accounting and tax purposes as an above the line (cost of goods sold) expense charged directly to the project. (Unless the rental equipment is used on more than one project, in which case, the rental fees are apportioned.)

The definition of PURCHASING an equipment asset is an “Agreement between buyer and seller to acquire an organization's assets. In an asset purchase, only specified assets transfer ownership from seller to buyer. Assets must be re-titled to the new owner who has the ability to determine which liabilities will be assumed. Unlike renting and leasing, the cost of the asset purchase is normally amortized over a period of time and asset are subject to depreciation expense.

06.5.3.04 - Types of Leases

The most common types of leases are operating leases and finance leases:

- Operating Lease - An operating lease is particularly attractive to companies that continually update or replace equipment and want to use equipment without ownership, but also want to return equipment at lease-end and avoid technological obsolescence. An operating lease usually results in the lowest payment of any financing alternative and is an excellent strategy for bypassing capital budgeting restraints. It typically qualifies for off-balance sheet treatment and can result in improved Return On Asset (ROA) due to a lower asset base. It can also result in higher reported earnings in the early years of the lease.

- Finance Lease - A finance lease is a full-payout, non-cancellable agreement, in which the lessee is responsible for maintenance, taxes and insurance. Finance leases are most attractive in cases where the lessee wants the tax benefits of ownership or expects the equipment's residual value to be high. These leases are structured as equipment financing agreements with residuals up to 10 percent. The lessee purchases the equipment upon lease termination at a pre-agreed amount. The term of a finance lease tends to be longer, nearly covering the useful life of the equipment.

Other types of leases are listed below:

Capital Lease - Type of lease classified and accounted for by a lessee as a purchase and by the lessor as a sale or financing, if it meets any one of the following criteria:

- the lessor transfers ownership to the lessee at the end of the lease term;

- the lease contains an option to purchase the asset at a bargain price;

- the lease term is equal to 75 percent or more of the estimated economic life of the property (exceptions for used property leased toward the end of its useful life); or

- the present value of minimum lease rental payments is equal to 90 percent or more of the fair market value of the leased asset less related investment tax credits retained by the lessor.

Direct Financing Lease (Direct Lease) - A non-leveraged lease by a lessor (not a manufacturer or dealer) in which the lease meets any of the definitional criteria of a capital lease, plus certain additional criteria.

First Amendment Lease - The first amendment lease gives the lessee a purchase option at one or more defined points with a requirement that the lessee renew or continue the lease if the purchase option is not exercised. The option price is usually either a fixed price intended to approximate fair market value or is defined as fair market value determined by lessee appraisal and subject to a floor to insure that the lessor's residual position will be covered if the purchase option is exercised. If the purchase option is not exercised, then the lease is automatically renewed for a fixed term (typically 12 or 24 months) at a fixed rental intended to approximate fair rental value, which will further reduce the lessor's end-of-term residual position. The lessee is not permitted to return the equipment on the option exercise date. If the lease is automatically renewed, then at the expiration of that initial renewal term, the lessee typically has the right either to return the equipment without penalty or to renew or purchase at fair market value.

Full Payout Lease - A lease in which the lessor recovers, through the lease payments, all costs incurred in the lease plus an acceptable rate of return, without any reliance upon the leased equipment's future residual value.

Guideline Lease - A lease written under criteria established by the IRS to determine the availability of tax benefits to the lessor.

Leveraged Lease - In this type of lease, the lessor provides an equity portion (usually 20 to 40 percent) of the equipment cost and lenders provide the balance on a nonrecourse debt basis. The lessor receives the tax benefits of ownership.

Net Lease - A lease wherein payments to the lessor do not include insurance and maintenance, which are paid separately by the lessee.

Open-end Lease - A conditional sale lease in which the lessee guarantees that the lessor will realize a minimum value from the sale of the asset at the end of the lease.

Sales-type Lease - A lease by a lessor who is the manufacturer or dealer, in which the lease meets the definitional criteria of a capital lease or direct financing lease.

Synthetic Lease - A synthetic lease is basically a financing structured to be treated as a lease for accounting purposes, but as a loan for tax purposes. The structure is used by corporations that are seeking off-balance sheet reporting of their asset based financing, and that can efficiently use the tax benefits of owning the financed asset.

Tax Lease - A lease wherein the lessor recognizes the tax incentives provided by the tax laws for investment and ownership of equipment. Generally, the lease rate factor on tax leases is reduced to reflect the lessor's recognition of this tax incentive.

Trac Lease - A tax-oriented lease of motor vehicles or trailers that contains a terminal rental adjustment clause and otherwise complies with the requirements of the tax laws.

True Lease - A type of transaction that qualifies as a lease under the Internal Revenue Code. It allows the lessor to claim ownership and the lessee to claim rental payments as tax deductions.

“Wet” or “Dry” leases - A “Wet Lease” is a leasing agreement that provides multiple services to the individual(s) leasing the aircraft, boat or other piece of equipment or machinery. This type of lease typically applies to the airline industry and under this agreement the owner will provide a crew, maintenance, and other services needed for the aircraft. While developed by the airline industry it has proven to be a popular model for specialized equipment such as ultra-heavy lift cranes and tunnel boring equipment Conversely, a “Dry Lease” is a type used for aircraft or any other equipment or machinery leasing in which the lessee arranges and pays for the crew, fuel, and maintenance. In marine terms it is called a bareboat charter.

- Montana State University Rent vs Lease vs Purchase Calculator http://tinyurl.com/pukhtv9

- RB Ritche Bros. (2014) When to buy or rent heavy equipment – five factors to consider.

- https://www.rbauction.com/blog/when-to-buy-or-rent-heavy-equipment-%E2%…-

- Shultz, Becky (2010) Options to Put You in the Operator's Seat http://www.forconstructionpros.com/article/10289086/buy-rent-or-lease-e…

06.5.3.05 - Salvage Value

Salvage Value is the estimated residual value of a depreciable asset or property at the end of its economic or useful life. In all methods for determining depreciation (except the double declining balance depreciation method) salvage value is deducted from the asset's purchase price. When the cost of an asset less its accumulated depreciation equals its salvage value, no more depreciation may be taken.

06.5.3.06 - Depreciation

Depreciating is a term which has several uses. The most common, especially as it relates to equipment is the Accounting definition, which states: The gradual conversion of the cost of a tangible capital asset or fixed asset into an operational expense (called depreciation expense) over the asset's estimated useful life. The objectives of computing depreciation are to:

(1) Reflect reduction in the book value of the asset due to obsolescence or wear and tear,

(2) Spread a large expenditure (purchase price of the asset) proportionately over a fixed period to match revenue received from it, and

(3) Reduce the taxable income by charging the amount of depreciation against the company's total income. In effect, charging of depreciation means the recovery of invested capital, by gradual sale of the asset over the years during which output or services are received from it. Depreciation is computed at the end of an accounting period (usually a year), using a method best suited to the particular asset. When applied to intangible assets, the preferred term is amortization.

Other uses of the term “depreciation” which project control professionals should know and understand are :

- Commerce: The decline in the market value of an asset.

- Economics: The decrease in the economic potential of an asset over its productive or useful life.

- Foreign exchange: The reduction in the exchange value of a currency, either by a government or due to weakening of the underlying economy in a floating exchange rate system.

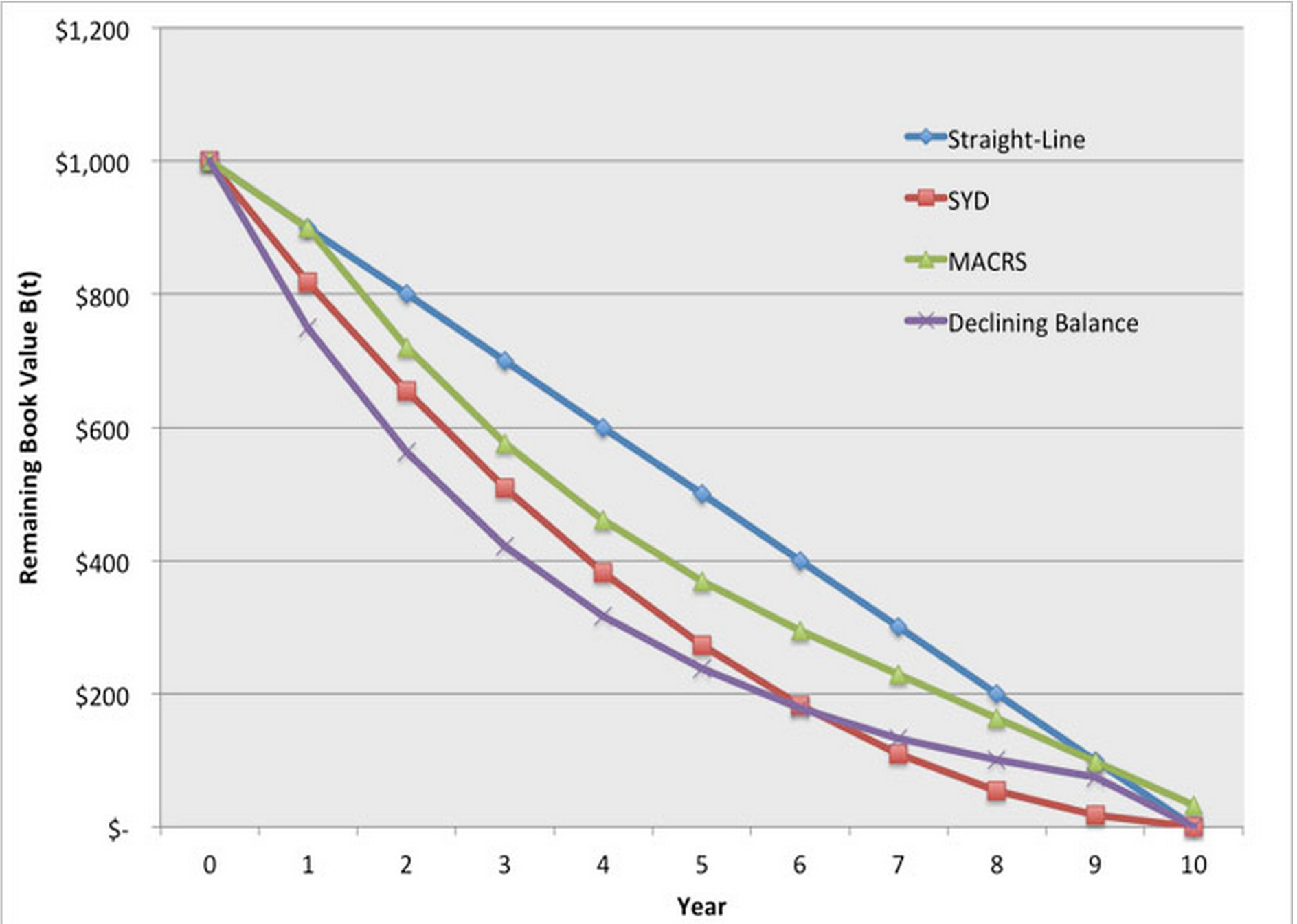

A project contrrols practitioner needs to know and understand the 4 most common deprecation methods, including knowing the formula and being able to solve a depreciation problem:

Figure 2 - Diagram showing the 4 most common depreciation methods

Source: Adapted from Building the Business Case (2016)

CASE STUDY:

The most straightforward depreciation method is straight-line depreciation. Under straight-line depreciation, the book value of an asset (less its salvage value, if any) can be depreciated evenly over some number of years. For example, if you had an asset with a book value of $1,000; no salvage value; and a ten-year depreciation horizon, you could claim $100 each year for ten years as a depreciation expense and tax deduction. ($1,000/10 years = $100 per year)

The other three depreciation methods that we will discuss here - sum of the year's digits, declining balance, and MACRS - are all forms of "accelerated depreciation." Under accelerated depreciation systems, a larger proportion of the asset's book value is allowed to be depreciated in the earlier years of its use, with smaller proportions depreciated in later years of use. This allows the asset owner to enjoy a lower tax burden earlier in the asset's life. Other things being equal, this leads to higher profits in the years immediately following investment. Accelerated depreciation can substantially affect the value of an asset to its owner; this re-allocation of tax burden and profits across the useful life of an asset increases the asset's lifetime benefit to its owner.

The three accelerated depreciation methods that we will illustrate in this lesson are:

(1) Sum of the Year's Digits (SYD): SYD is best illustrated using a simple example. Suppose that an asset could be depreciated over five years. Then the sum of the digits would be 1+2+3+4+5 = 15. The first year, you could claim 5/15 = 33% of the asset's book value as a depreciation expense, so that A(1) = 33%. The second year, the depreciation allowance would be A(2) = 4/15 = 27%. You can verify for yourself that A(3) = 20%; A(4) = 13%; and A(5) = 7%.

(2) Declining balance: This could also be called "exponential depreciation" since it depreciates an asset at a constant rate, rather than a constant amount. If an asset is depreciated using the declining balance method over a fixed number of years, the residual book value of the asset is used as the depreciation allowance in the final year. For example, if you had a $100 asset with no salvage value, and were claiming depreciation according to the declining balance system at 25% per year over five years, in the first year your depreciation allowance would be D(1) = 0.25 × $100 = $25. In the second year you would have D(2) = 0.25 × ($100 - $25) = 0.25 × $75 = $18.75. You can verify for yourself that D(3) = $14.06; D(4) = $10.55, and D(5) = $31.64.

(3) Modified Accelerated Cost Recovery: MACRS, popular in the United States, is embodied in a series of depreciation tables published by the U.S. Internal Revenue Service. The tables dictate the values of A(t) to be used each year, and also describe which types of assets are eligible for MACRS and over how many years. In other words, different asset types have different values of N and different depreciation schedules A(t). One odd thing about MACRS is that the N-year depreciation schedules actually cover N+1 years (so, for example, five-year MACRS allows depreciation over six years).

As a means of comparison between all of these methods, let's take a hypothetical asset with a book value of $1,000 and zero salvage value, and depreciate that asset over a ten year time horizon. Table 8.6 and Figure 8.1 show the values of B(t) during each year for each of the four methods. For declining balance, we will use 25% per year. For MACRS we are using the 10-year table in Appendix 1 of Publication 496.

06.5.4 - OUTPUTS

- OPTIMIZED SELECTION OF EQUIPMENT

- EQUIPMENT ACQUIRED

- EQUIPMENT ASSIGNED TO THE PROJECT

06.5.5 - REFERENCES & TEMPLATES

- CATERPILLAR PERFORMANCE HANDBOOK EDITION 29 HTTP://NEES.UCSD.EDU/FACILITIES/DOCS/PERFORMANCE_HANDBOOK_416C.PDF

- BLUMSACK, SETH (2014) DEPRECIATION ACCOUNTING HTTPS://WWW.E-EDUCATION.PSU.EDU/EME801/NODE/546

- DYMENT, ROBERT (1996) RENTING, LEASING, OR OWNING CONSTRUCTION EQUIPMENT HTTP://WWW.CONCRETECONSTRUCTION.NET/IMAGES/RENTING,%20LEASING,%20OR%20OWNING%20CONSTRUCTION%20EQUIPMENT_TCM45-343072.PDF

- US INTERNAL REVENUE SERVICE (IRS) (2014) PUBLICATION 946 CAT. NO. 13081F HOW TO DEPRECIATE PROPERTY HTTP://WWW.IRS.GOV/PUB/IRS-PDF/P946.PDF

- MACRS DEPRECIATION CALCULATOR BASED ON IRS PUBLICATION 946 (N.D.) HTTP://WWW.FREE-ONLINE-CALCULATOR-USE.COM/MACRS-DEPRECIATION-CALCULATOR.HTML#STHASH.8J9GR81E.DPUF

06.6 - Module 06-6 - Allocating Resources

GPCCAR M06-5 - Managing Resource Acquisition / Allocation, Revision 1.00